By Ovi

All of the Crude plus Condensate (C + C) production data, oil, for the US state charts comes from the EIAʼs Petroleum Supply monthly PSM which provides updated information up to June 2024.

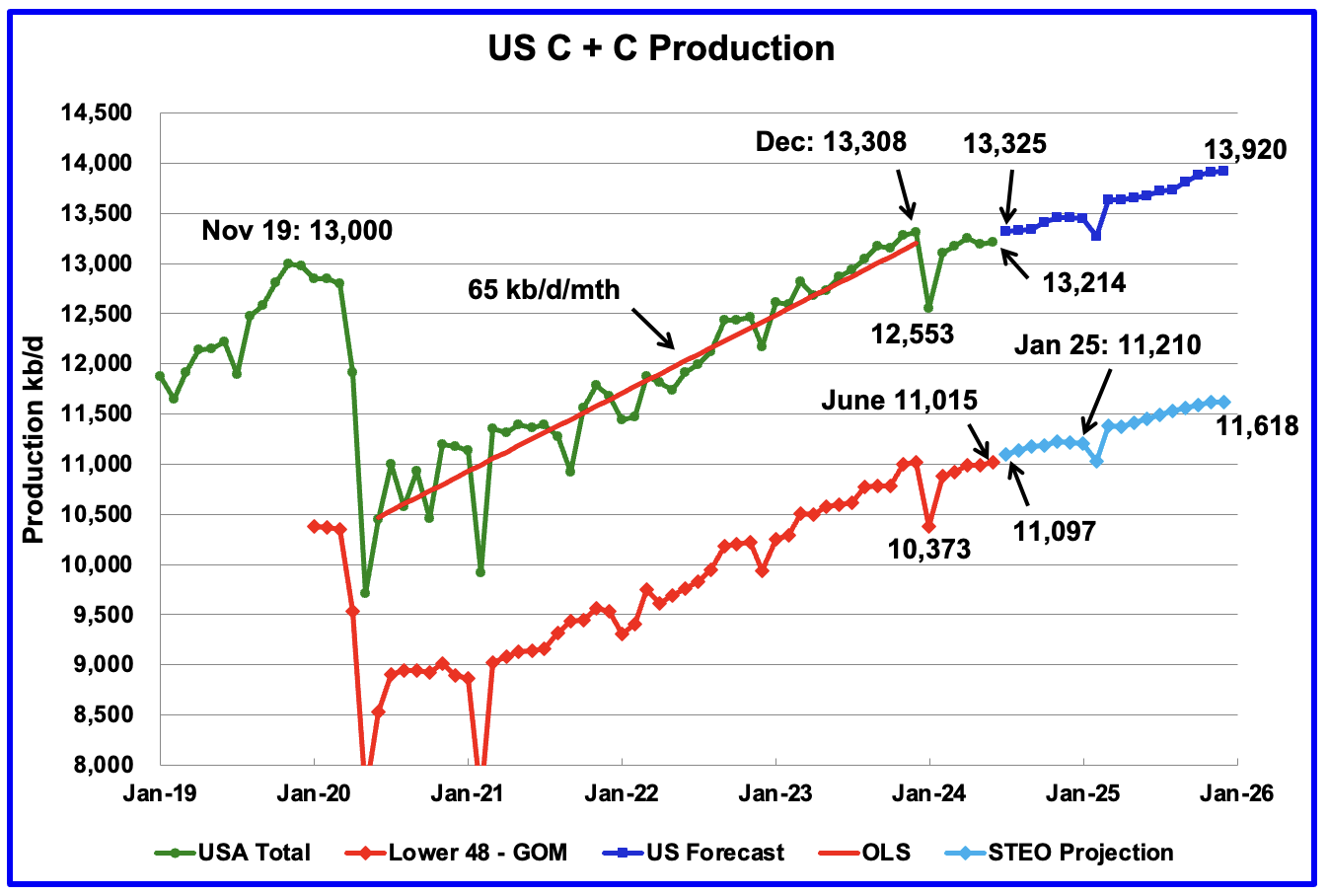

U.S. June oil production rose by 25 kb/d to 13,214 kb/d. The largest increase came from Texas, 58 kb/d while 7 states had production drops totalling 51 kb/d.

US oil production has been flat since November 2023 when it was 13,281 kb/d.

The dark blue graph, taken from the August 2023 STEO, is the forecast for U.S. oil production from July 2024 to December 2025. Output for December 2025 is expected to reach 13,920 kb/d which is a decrease of 89 kb/d from the previous STEO report.

From July 2024 to December 2025 production is expected to grow by 595 kb/d or at an average rate of 35 kb/d/mth.

The red OLS line from June 2020 to December 2023 indicates a monthly production growth rate of 65 kb/d/mth or 780 kb/d/yr. Production going forward is projected to increase at about 1/2 that rate.

The light blue graph is the STEO’s projection for output to December 2025 for the Onshore L48. From July 2024 to December 2025, production is expected to increase by 521 kb/d to 11,618 kb/d which is 108 kb/d kb/d lower than reported in the previous STEO.

US Oil Production Ranked by State

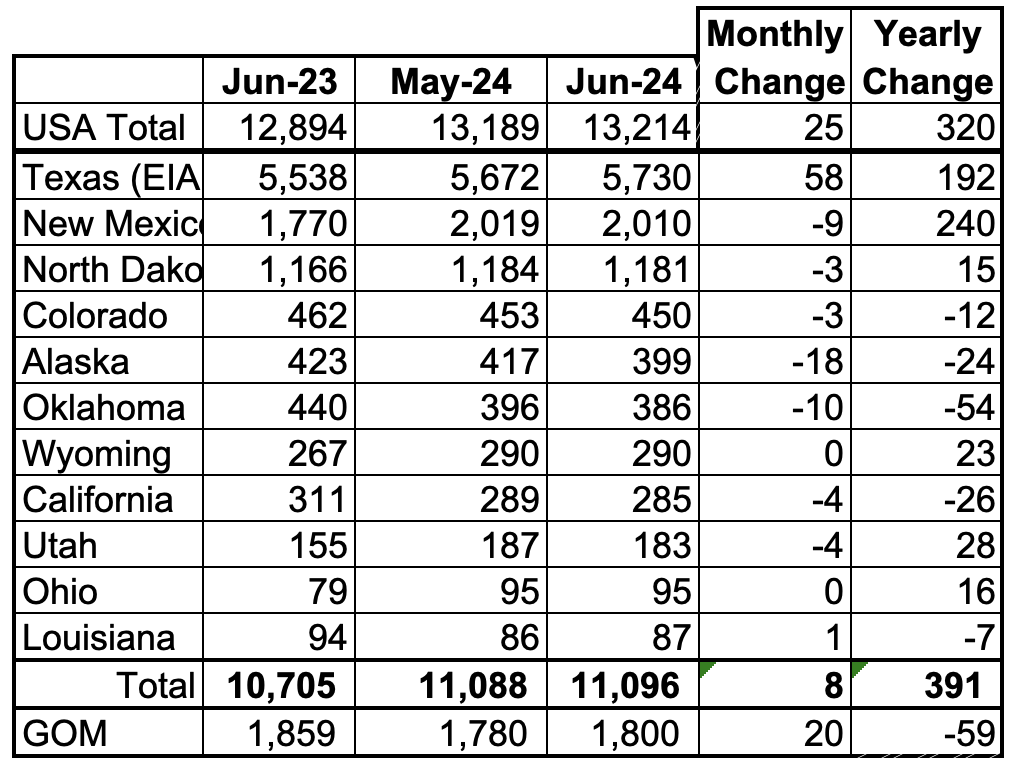

Listed above are the 11 US states with the largest oil production along with the Gulf of Mexico. Ohio has been added to this table since its production approached 100 kb/d in January and exceeded Louisiana’s production. These 11 states accounted for 84% of all U.S. oil production out of a total production of 13,214 kb/d in June 2024.

On a YoY basis, US production increased by 320 kb/d. GOM production decreased by 20 kb/d MoM while YoY it dropped by 59 kb/d.

State Oil Production Charts

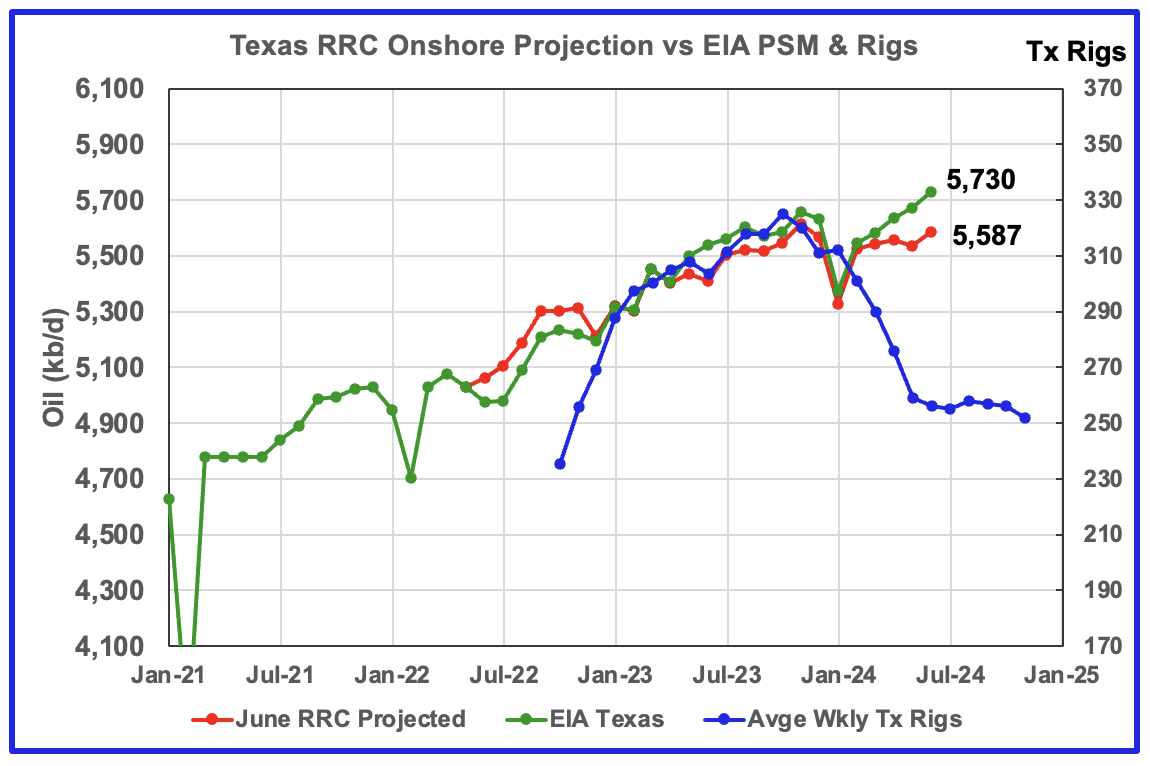

Texas production increased by 58 kb/d in May to 5,730 kb/d. YoY production is up by 192kb/d.

The red graph is a production projection for Texas using the Texas RRC reported May and June oil production. The projection uses the cumulative difference between the May and June preliminary production data provided by the Texas RRC. The projection does not provide a reasonable estimate for Texas’ June production vs the EIA’s official 5,730 kb/d.

In checking oil production from Texas counties, it was found that a number of them had a significant production drop in May, which could be due to either a delay in reporting or a processing delay by the Texas RRC. The late/low reporting of May causes the June upswing to 5,587 kb/d. It is not clear and surprising why the production projection after January 2024 is showing an ever widening gap with the EIA, considering the close results for February and the prior months.

The blue line is the average numbers of weekly rigs reported for each month, shifted forward by 9 months. So the 276 rigs operating in July 2023 have been shifted forward to April 2024. So if production should follow the rig count, Texas production should begin to decline shortly.

According to the EIA, New Mexico’s June production dropped by 9 kb/d to 2,010 kb/d.

The blue graph is a production projection for Lea plus Eddy counties. These two counties account for close to 99% of New Mexico’s oil production. The projection used the difference between the May and June preliminary production data provided by the New Mexico Oil Conservation Division. The projection provides a reasonable estimate for New Mexico’s January to June production. A 1% correction was added to the Lea plus Eddy projection to account for their fraction of New Mexico’s oil production.

Note the methodology used to project New Mexico’s production is the same as that used for Texas. This raises the question of why are the New Mexico results so much closer to the EIA’s data than Texas?

More oil production information for these two counties and Texas counties is reviewed in the special Permian section further down.

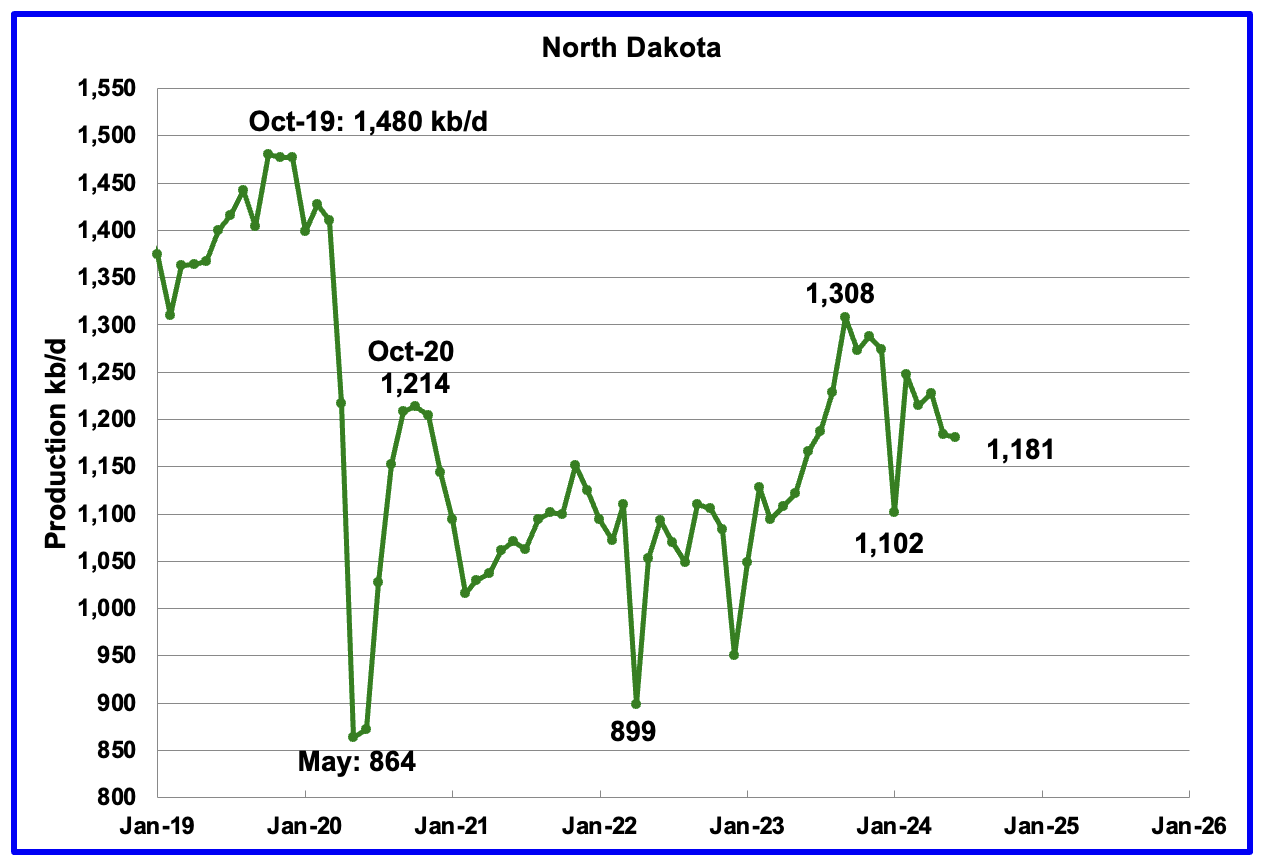

June’s output decreased by 3 kb/d to 1,181 kb/d. YoY production was up by 15 kb/d. The North Dakota DMR reported that oil production dropped by 22 kb/d in June to 1,176 kb/d.

According to this article, North Dakota’s oil production dropped in June.

“In the latest Director’s Cut report, Department of Mineral Resources Assistant Director Mark Bohrer said oil production fell 2% to about 1.17 million barrels per day. Gas production saw a 1% drop to about 3.47 billion cubic feet of gas a day.

He said it may be difficult to achieve the 1.3 million barrel mark by the end of the year, given the slow movement trends.”

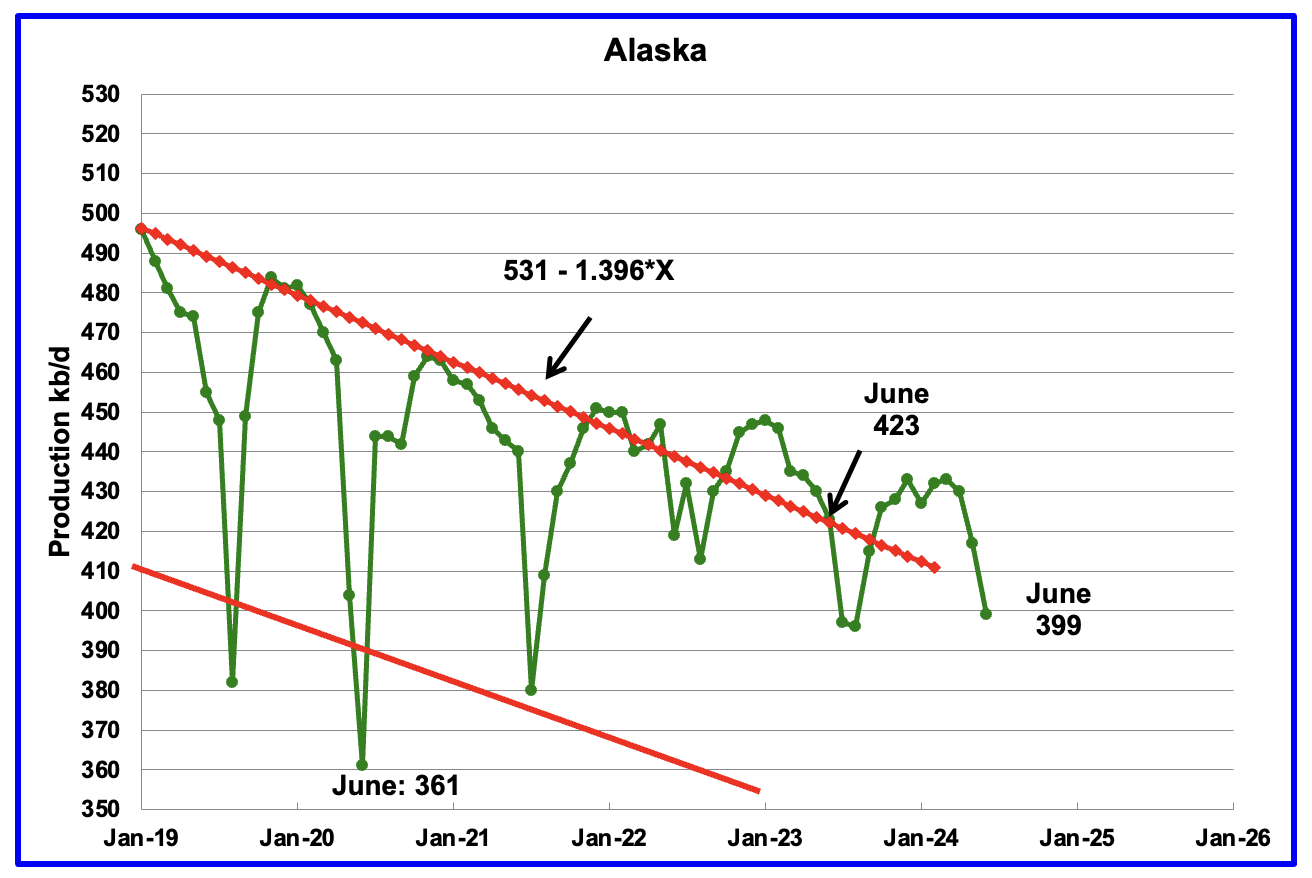

Alaskaʼs June output dropped by 18 kb/d to 399 kb/d. Production YoY is also down by 24 kb/d. The EIA’s weekly petroleum report continues to show Alaska’s July oil production also dropping below 400 kb/d. Typically Alaska’s production drops in the summer months due to maintenance.

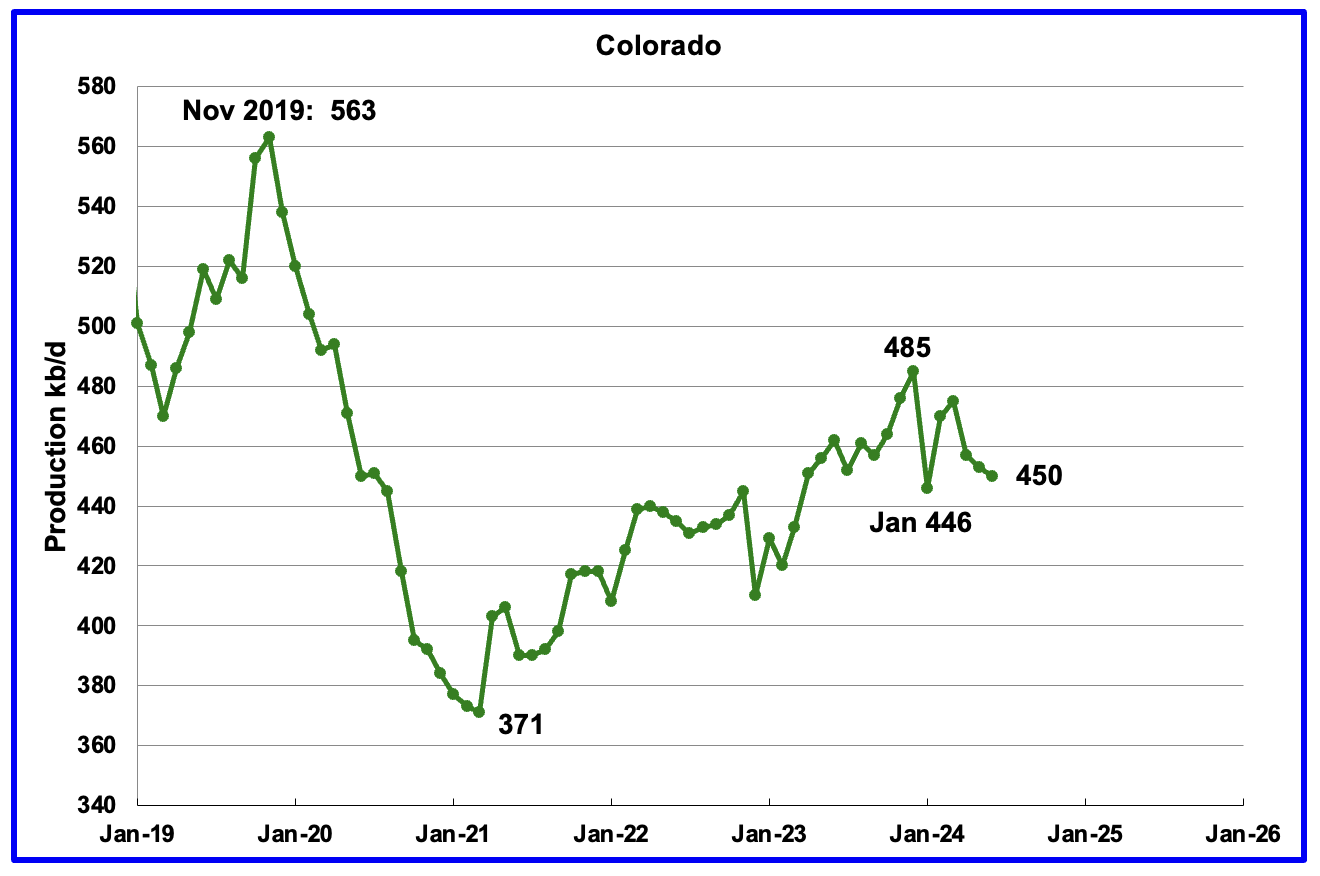

Coloradoʼs June oil production decreased by 3 kb/d to 450 kb/d. Colorado has moved ahead of Alaska to become the 4th largest US oil producing state. Colorado began the year with 12 rigs but has now dropped to 10 during June, July and August.

Oklahoma’s output in June dropped by 10 kb/d to 386 kb/d. Production remains below the post pandemic July 2020 high of 476 kb/d. Output appears to have entered a slow declining phase in June 2023. Oklahoma’s rig count dropped from 40 in May to 30 in July. By the end of August there was an uptick to 37 operational rigs. Will increase in the rig count reverse the current dropping production trend?

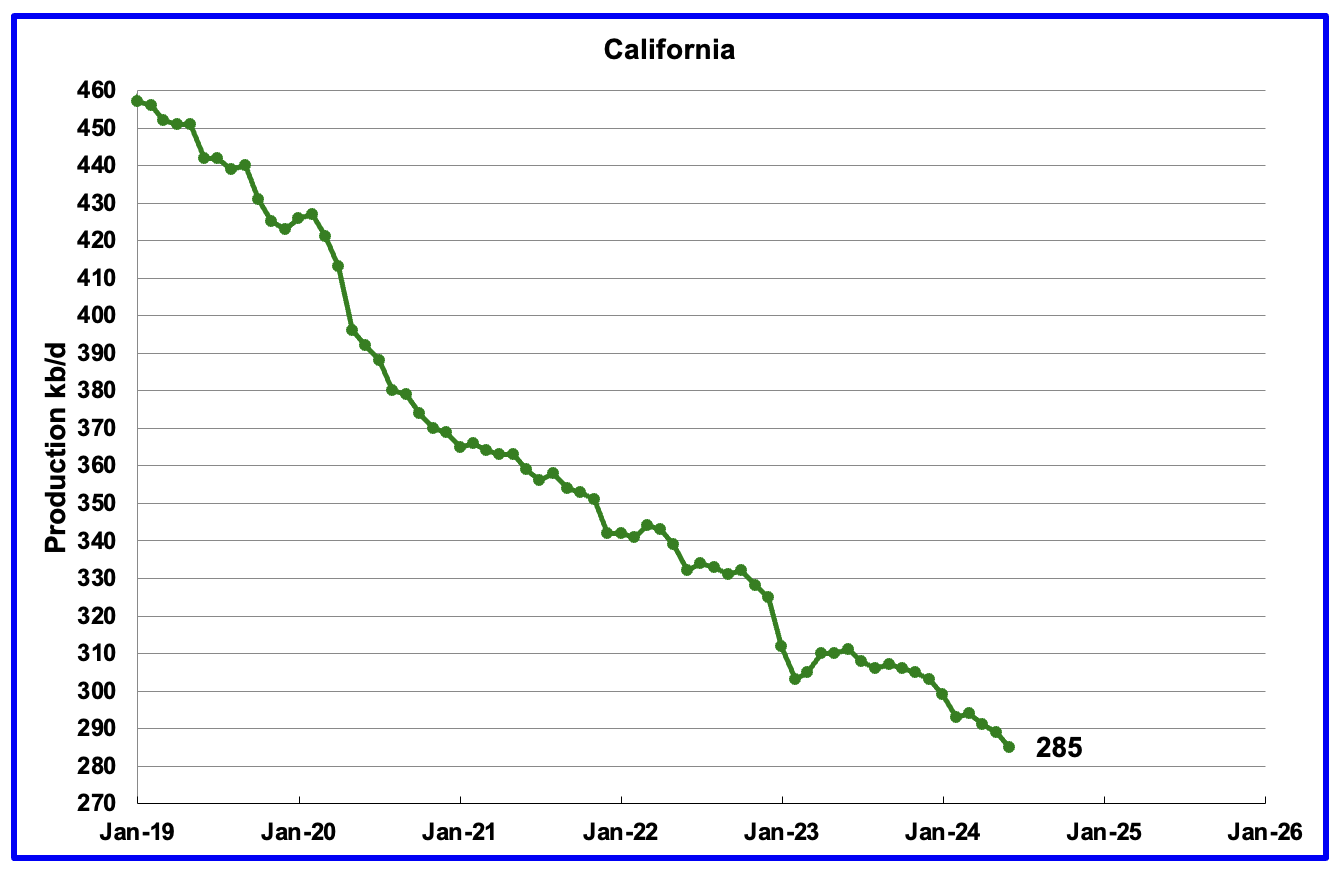

California’s declining production trend continues. Californiaʼs June production dropped by 4 kb/d to 285 kb/d.

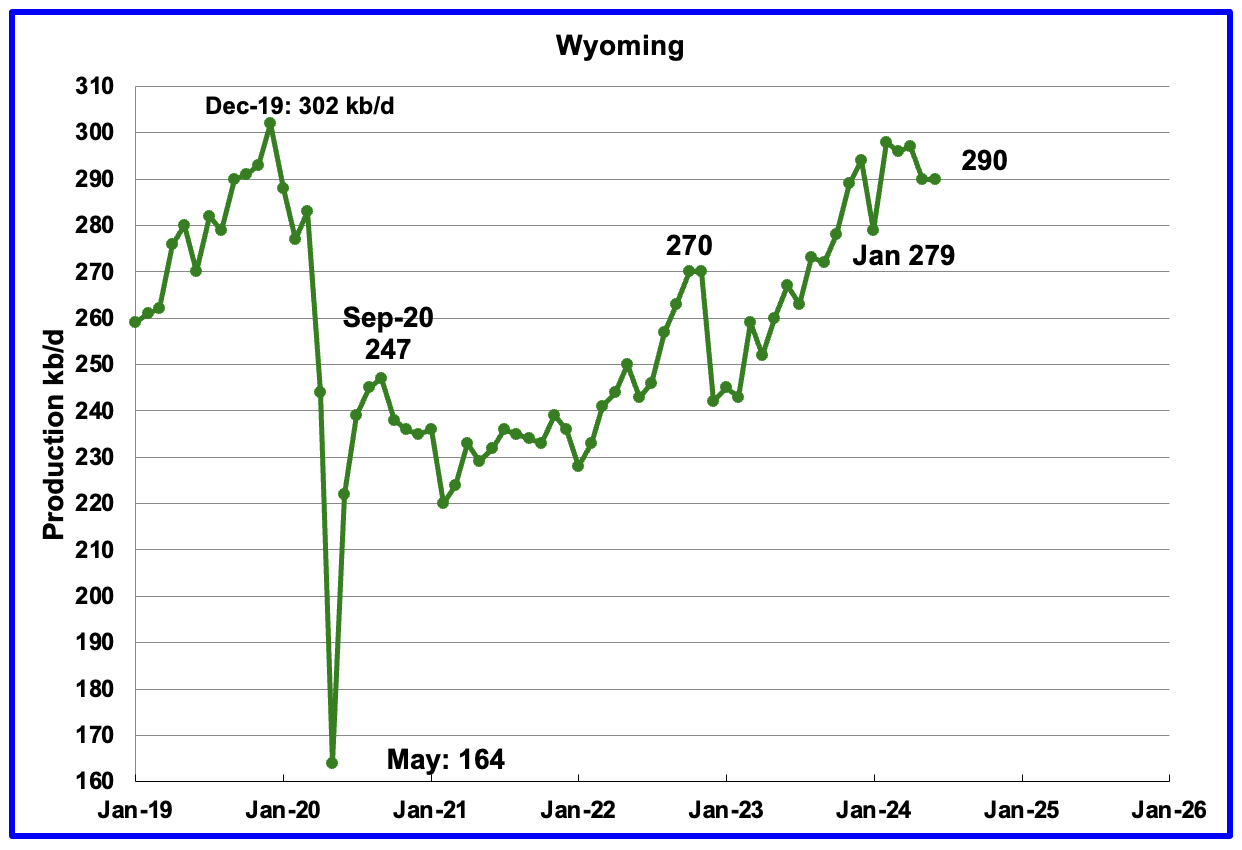

Wyoming’s oil production has been rebounding since March 2023. However the rebound was impacted by the January 2024 storm. June production was flat at 290 kb/d and may be entering a plateau phase. Note that production has almost recovered to the pre-Covid level.

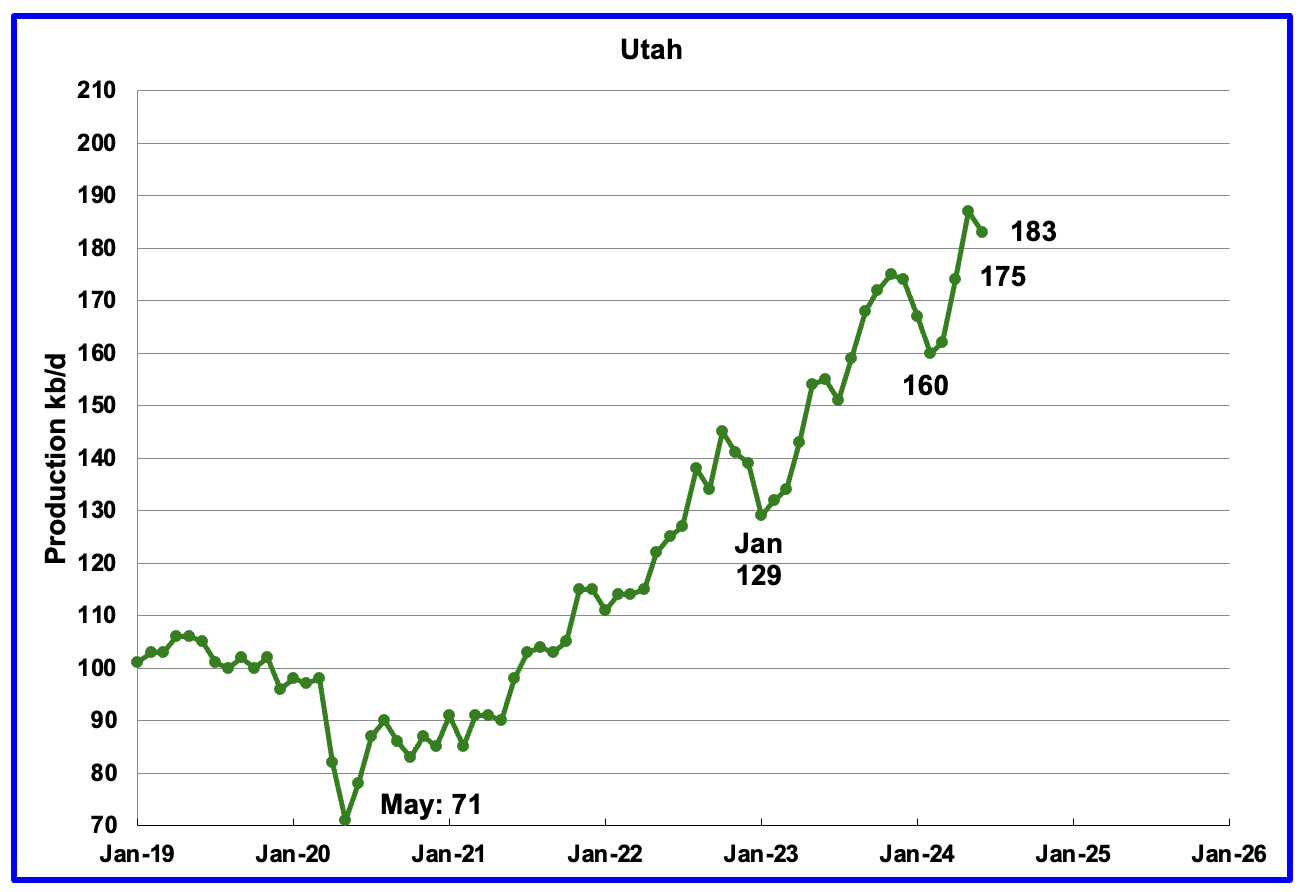

June’s production decreased by 4 kb/d to 183 kb/d. Utah has had 9 oil rigs in operation through out 2024.

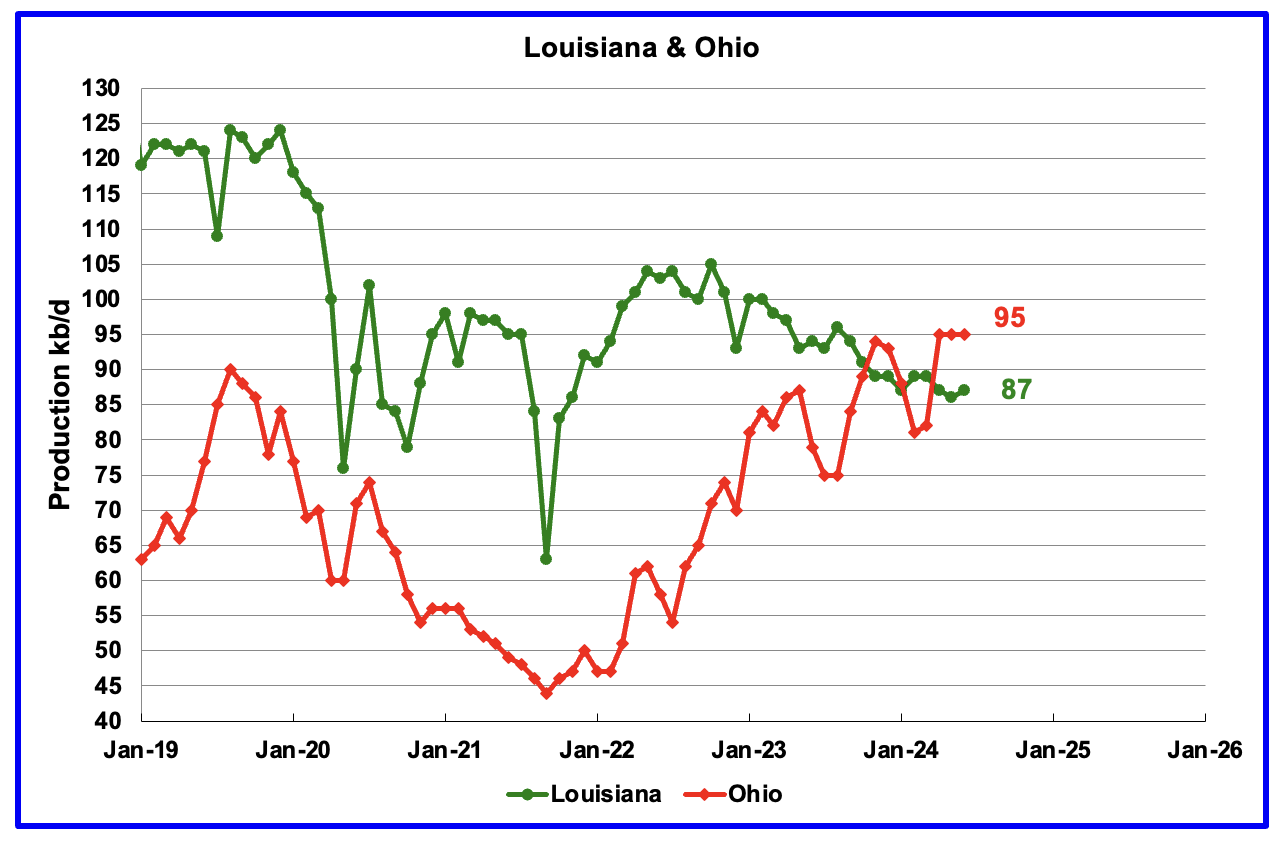

Ohio has been added to the Louisiana chart because Ohio’s production has been slowly increasing since October 2021 and passed Louisiana in November 2023.

Louisiana’s output entered a slow decline phase in October 2022. June’s production increased by 1 kb/d to 87 kb/d. Ohio’s oil production was flat at 95 kb/d, a new high. The most recent Baker Hughes rig report now shows two horizontal oil rigs operating in Ohio in July and August.

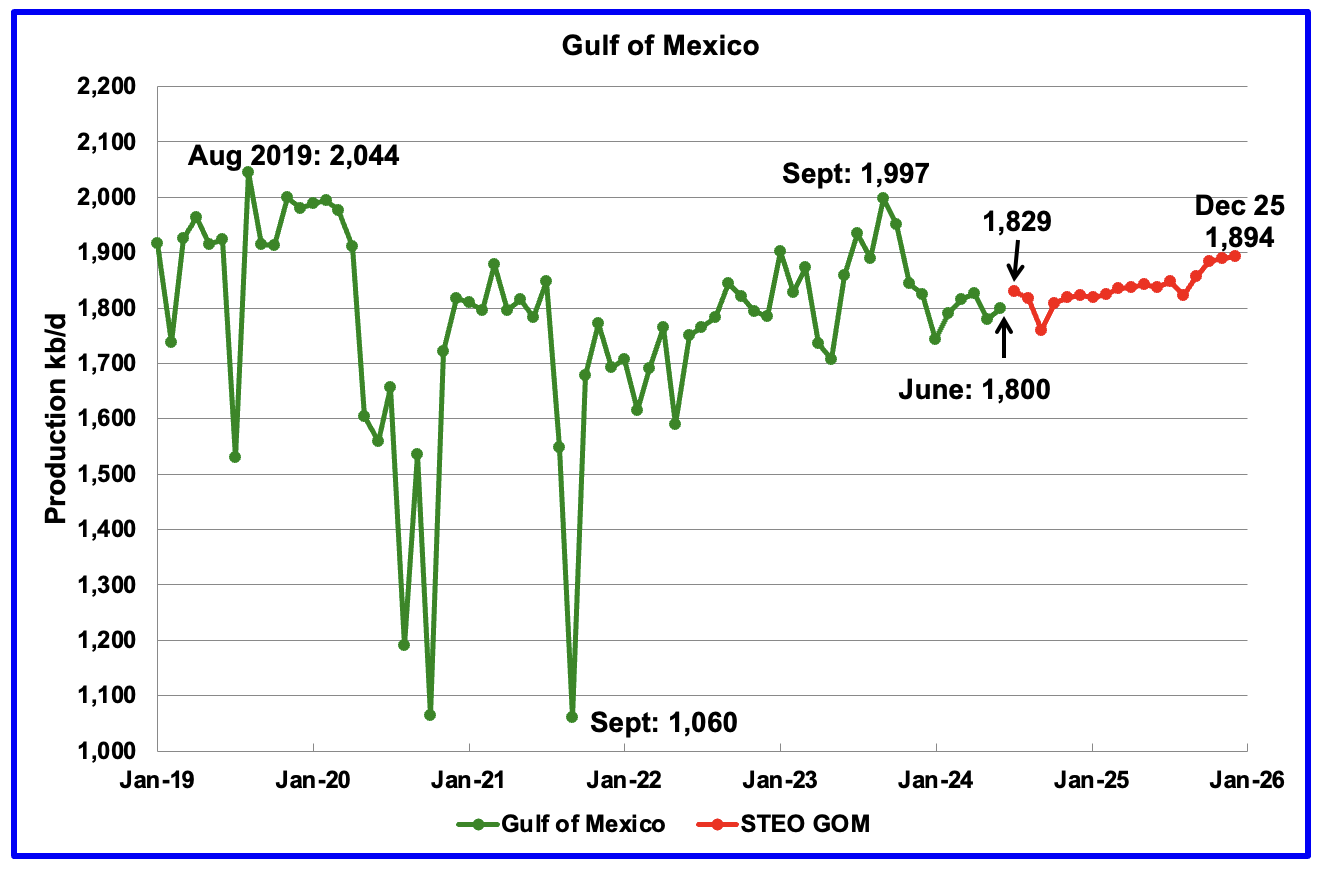

GOM production rose by 20 kb/d in June to 1,800 kb/d but is expected to rise by 29 kb/d in July to 1,829 kb/d.

The August 2024 STEO projection for the GOM output has been added to this chart. It projects production from July 2024 to December 2025 will rise by 65 kb/d to 1,894 kb/d which is 19 kb/d higher than in the previous STEO.

In the January 2024 EIA report, the STEO was forecasting December 2025 GOM oil production to be 1,954 kb/d, 125 kb/d higher than the latest forecast. What changed? It could change again according to the article below.

According to this article and this article, Chevron has made a significant breakthrough in the GOM.

Chevron breakthrough a boon for deepwater US Gulf

New York, 3 September (Argus) — The start-up of the first ultra-high pressure deepwater development in the US Gulf of Mexico paves the way for millions of barrels of previously hard-to-reach resources to be tapped in the offshore basin.

First oil from Chevron’s $5.7bn, 75,000 b/d Anchor project — designed to withstand pressures of up to 20,000 lb/inch² (1,400 kg/cm²) with reservoir depths reaching 34,000ft (10,400m) below sea level — opens up a new frontier in deepwater production. Not only will it increase output from a region where production has plateaued since peaking at 2mn b/d in 2019, but the expertise gleaned could also be deployed in prospects from Namibia to Brazil.

The so-called “20k” high-pressure technology could potentially unlock more than 2bn boe of resources in the US Gulf of Mexico, consultancy Wood Mackenzie says. Operators expect individual wells to recover at least 30mn boe, which could extend the operating life of the basin. Chevron, one of the largest leaseholders in the deepwater Gulf of Mexico, has three projects due to come on line in the area after Anchor. “However, if results fall short, it could mark the beginning of a production decline in the basin and a blow to a resurgence in exploration for additional barrels in the play,” Wood Mackenzie principal analyst Mfon Usoro says.

A Different Perspective on US Oil Production

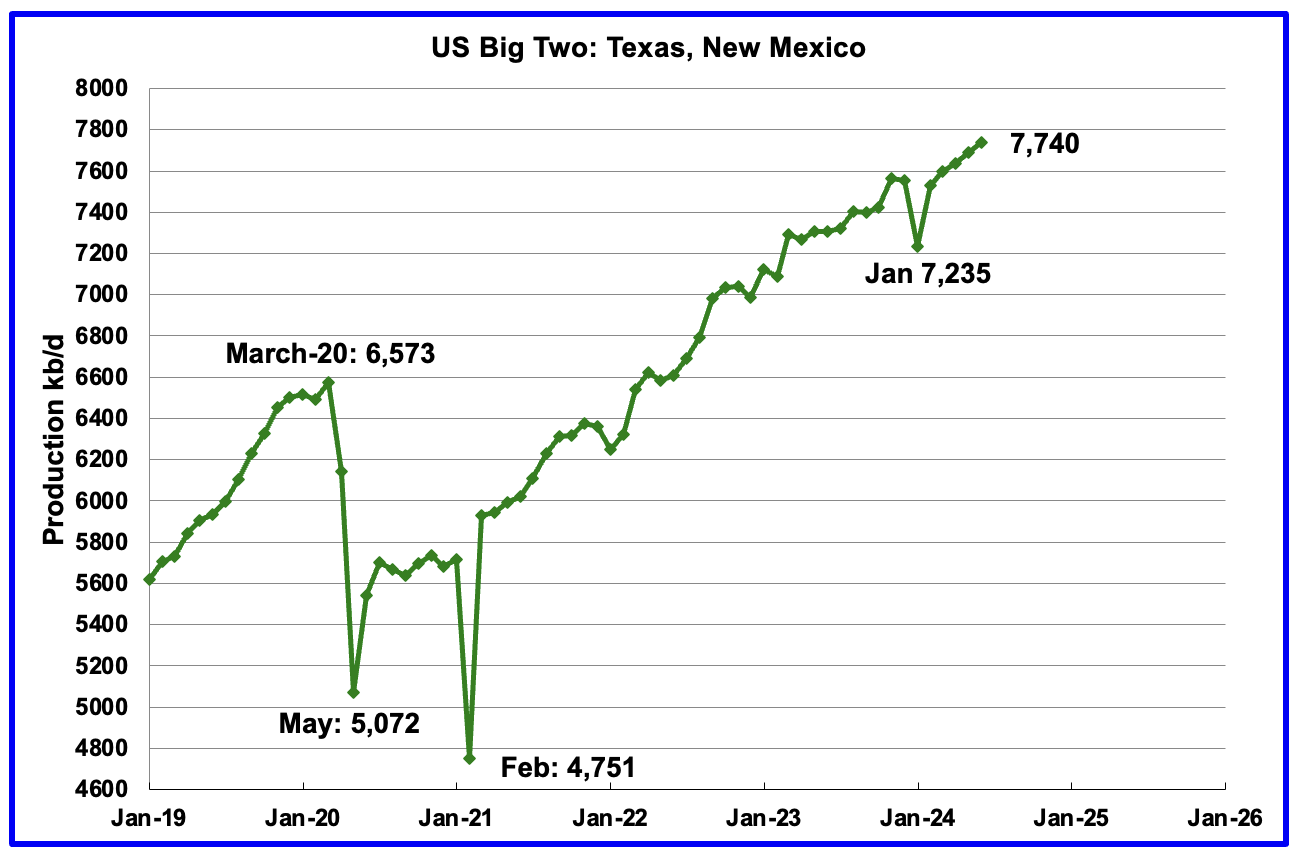

The Big Two states combined oil output for Texas and New Mexico.

June’s production in the Big Two states increased by a combined 49 kb/d to 7,740 kb/d with Texas adding 58 kb/d while New Mexico dropped 9 kb/d.

Oil production by The Rest

June’s oil production in The Rest dropped by 26 kb/d to 3,275 kb/d and is 184 kb/d lower than November 2023.

The main takeaway from The Rest chart is that current production is below the high of October 2019 and is a significant loss that occurred during the Covid shut down and will not be readily recovered. Note that production is now lower than Sept 2020 post covid rebound to 3,302 kb/d.

The On-Shore lower 48 W/O the big three, Texas, New Mexico and North Dakota, shows production is on a plateau in the range of 2,100 ±100 kb/d from January 2023.

June’s production decreased by 23 kb/d to 2,094 kb/d. Two of the bigger contributors with declines were Alaska 18 kb/d and Oklahoma 10 kb/d.

Permian Basin Report by Main Counties and Districts

This special monthly Permian section was recently added to the US report because of a range of views on whether Permian production will continue to grow or will peak over the next year or two. The issue was brought into focus recently by the Goehring and Rozencwajg Report which indicated that a few of the biggest Permian oil producing counties were close to peaking or past peak. Also comments by posters on this site have similar beliefs from hands on experience.

This section will focus on the four largest oil producing counties in the Permian, Lea, Eddy, Midland and Martin. It will track the oil and natural gas production and the associated Gas Oil Ratio (GOR) on a monthly basis. The data is taken from the state’s government agencies for Texas and New Mexico. Typically the data for the latest two or three months is not complete and is revised upward as companies submit their updated information. Note the natural gas production shown in the charts that is used to calculate the GOR is the gas coming from both the gas and oil wells.

Of particular interest will be the charts which plot oil production vs GOR for a county to see if a particular characteristic develops that indicates the field is close to entering or in the bubble point phase. While the GOR metric is best suited for characterizing individual wells, counties with closely spaced horizontal wells may display a behaviour similar to individual wells due to pressure cross talking . For further information on the bubble point and GOR, there are a few good thoughts on the intricacies of the GOR in an earlier POB comment. Also check this EIA topic on GOR.

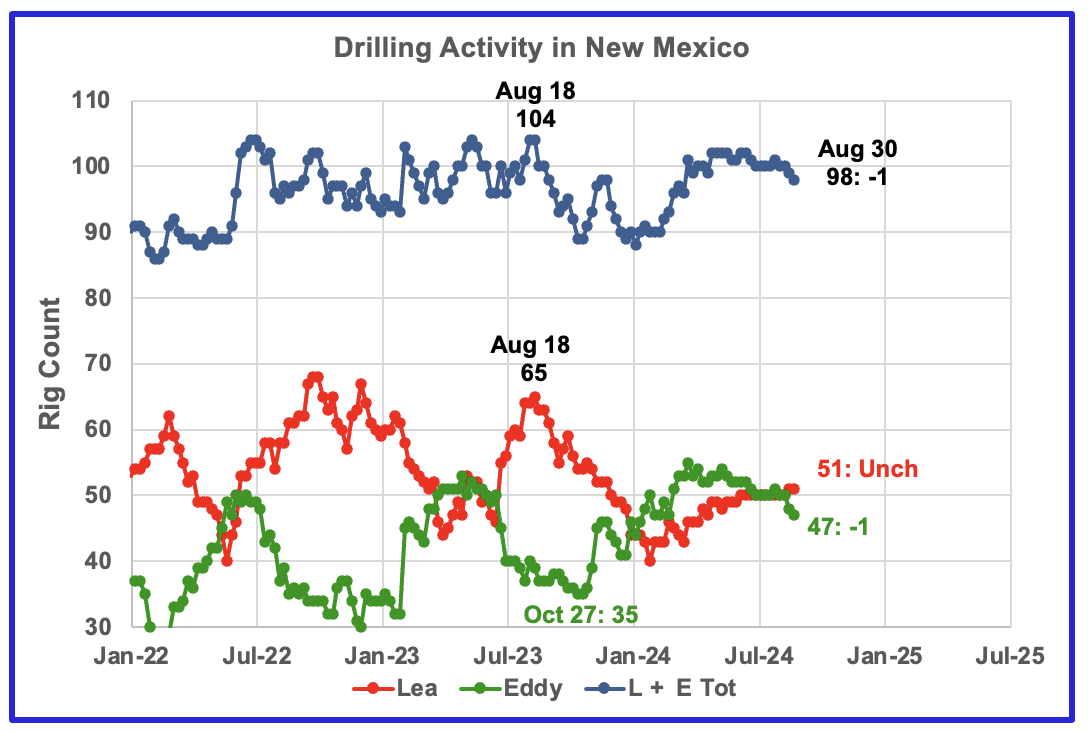

New Mexico Permian

The rig count in late August 2024 is down 6 from the August 2023 high of 104 rigs.

Since the middle of August 2023, the Lea county rig count has dropped from 65 rigs to 40 rigs in late January 2024. Since then the rig count has slowly risen by 11 to 51 rigs at the end of August. At the same time production has increased to 1,250 kb/d over the period January 2023 to June 2024. However due to a time lag between rig count and production, Lea may be on the verge of entering a decline phase. See next chart.

From a low of 35 rigs in late October 2023, 20 rigs were transferred into Eddy county between October and March 2024. At its peak in late March 2024, Eddy county had 55 rigs operating and are now down to 47 rigs at the end of August.

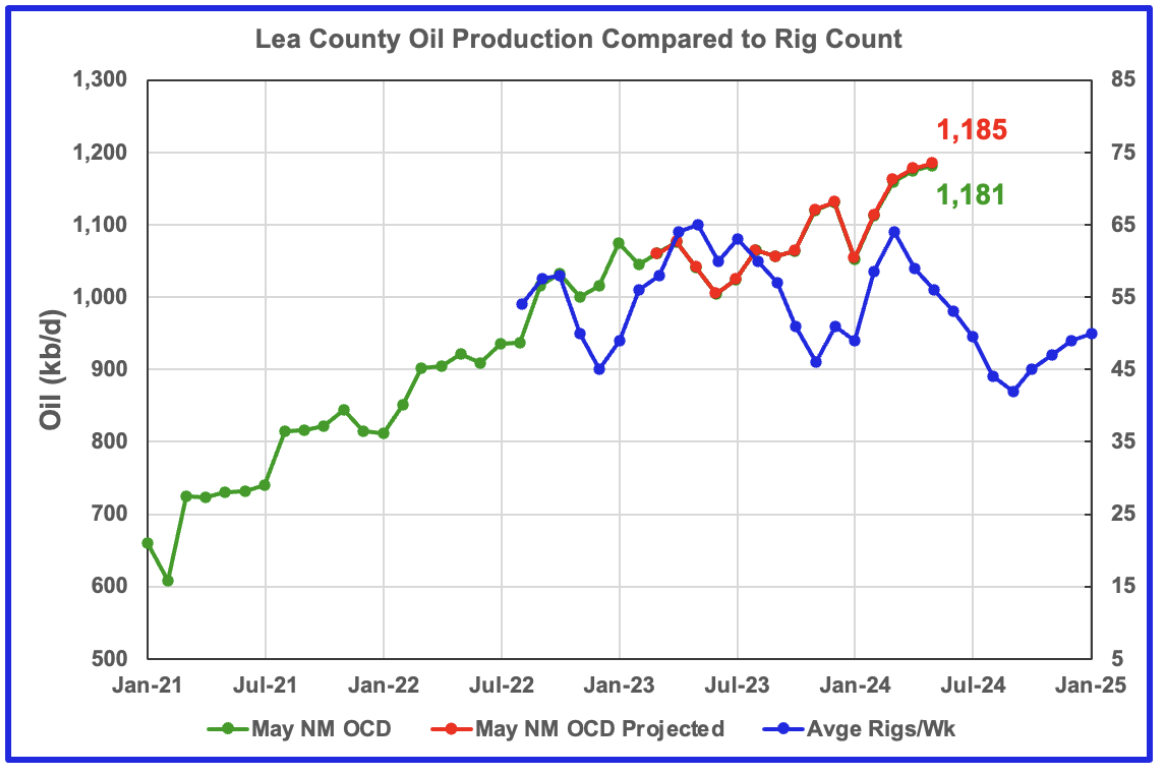

For comparison to the chart below, last month’s Lea oil production chart.

This chart is indicating that we will have to wait for another month or two to determine how close Lea county is to peaking.

The June update made a total upward revision of 48 kb/d to production between the months March 2023 to June 2023. This revision shifted both the original June OCD data and the projection upward and created a big gap between the June data and the projection. The previous posts showed almost no changes between the original data and the projection after one year, see comparison chart above.

While the latest June New Mexico OCD data shows a big drop in June production, the upward production revisions of 48 kb/d along with the typical previous month production drop results in a 20 kb/d increase in the projected June production. While this is what the model forecasts, I don’t think it is correct and it will be sorted out next month, provided the production revisions are more typical.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the weekly rig chart. The rig graph has been shifted forward by 8 months. So the 64 Rigs/wk operating in August 2023 have been time shifted forward to April 2024 to show the possible correlation and time delay between rig count and oil production.

Note that rig counts are being used to project production as opposed to completions because very few extra DUCs are being completed at this time.

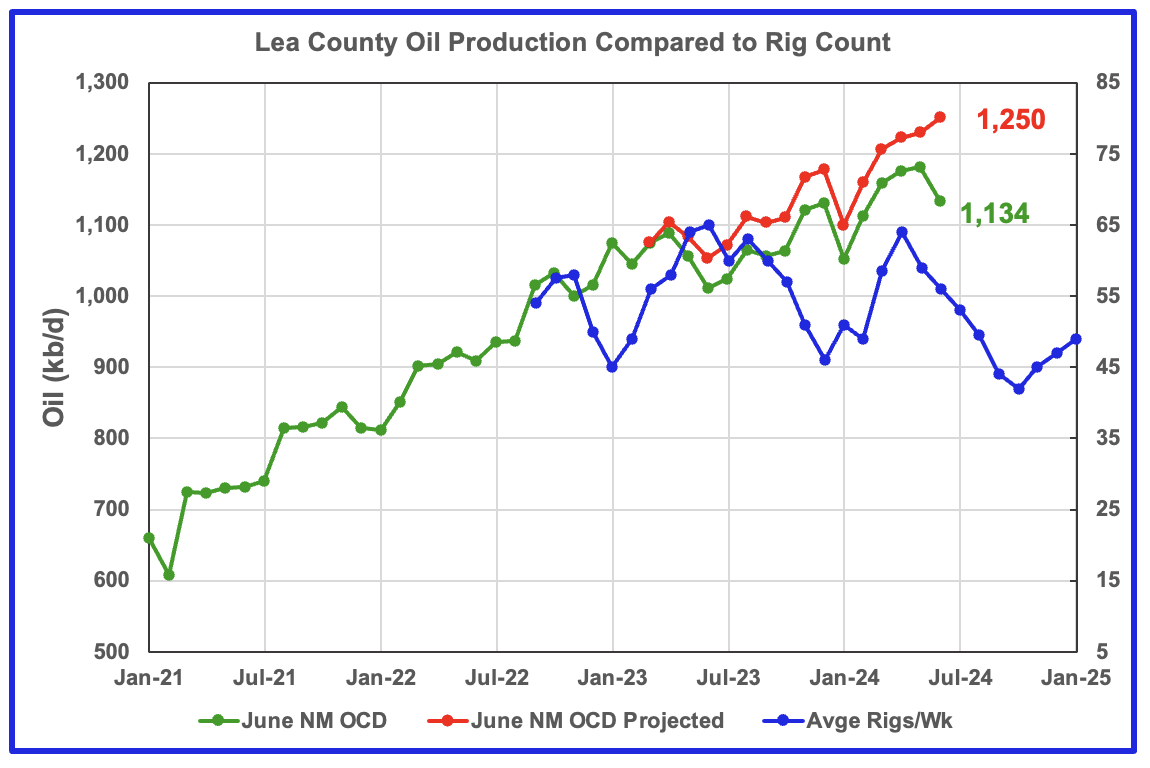

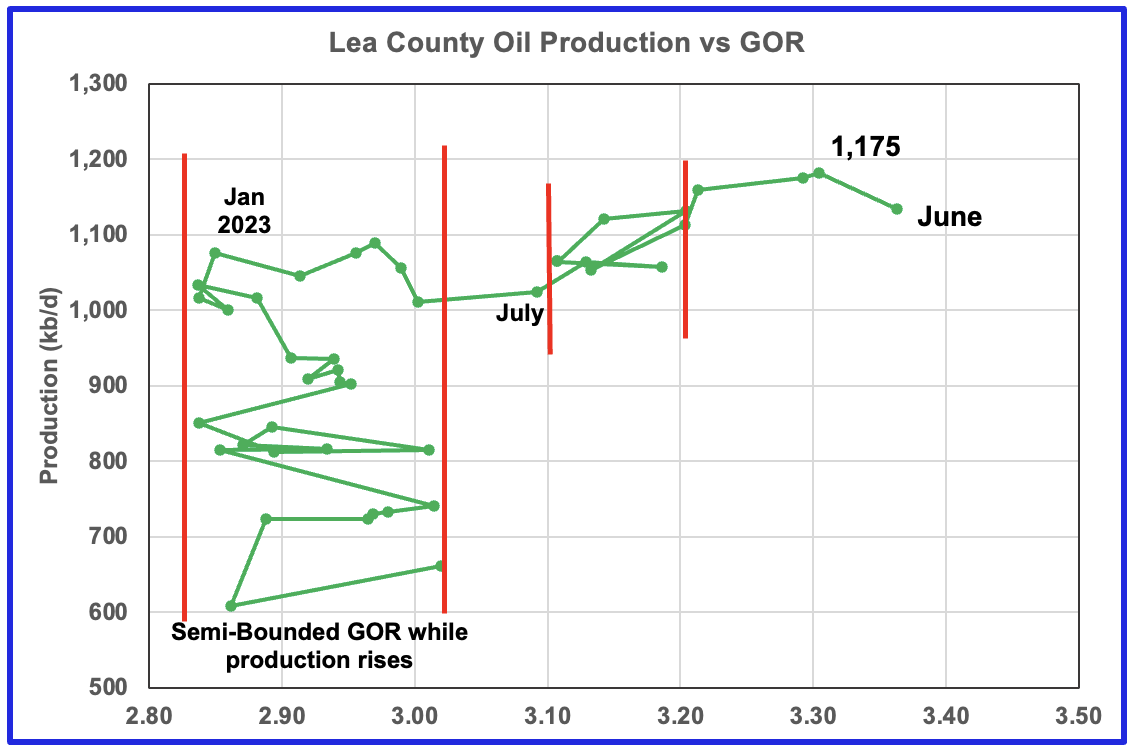

After much zigging and zagging, oil production in Lea county stabilized just above 1,000 kb/d in early 2023. Once production reached a new high in January 2023, production rose more slowly while the GOR started to increase rapidly to the right and entered the bubble point phase in July 2023.

Since July 2023 Lea county GOR has continued to increase as production increased. This may indicate that the current production increase is coming from a new bench/area since the GOR’s behaviour since August 2023 to March 2024 time frame appears once again to be in a semi bounded GOR phase accompanied with rising production. However in April, May and June 2024, the GOR moved out of the Second semi bounded GOR region and production reached a new high 1,175 kb/d in May along with an another increase in the GOR. The increase in the GOR for the last three months is another indicator that Lea county has entered the bubble point phase for a second time and that production is near its peak.

This zigging and zagging GOR pattern within a semi-bounded GOR while oil production increases to some stable level and then moves out to a higher GOR to the right has shown up in a number of counties. See an additional two cases below.

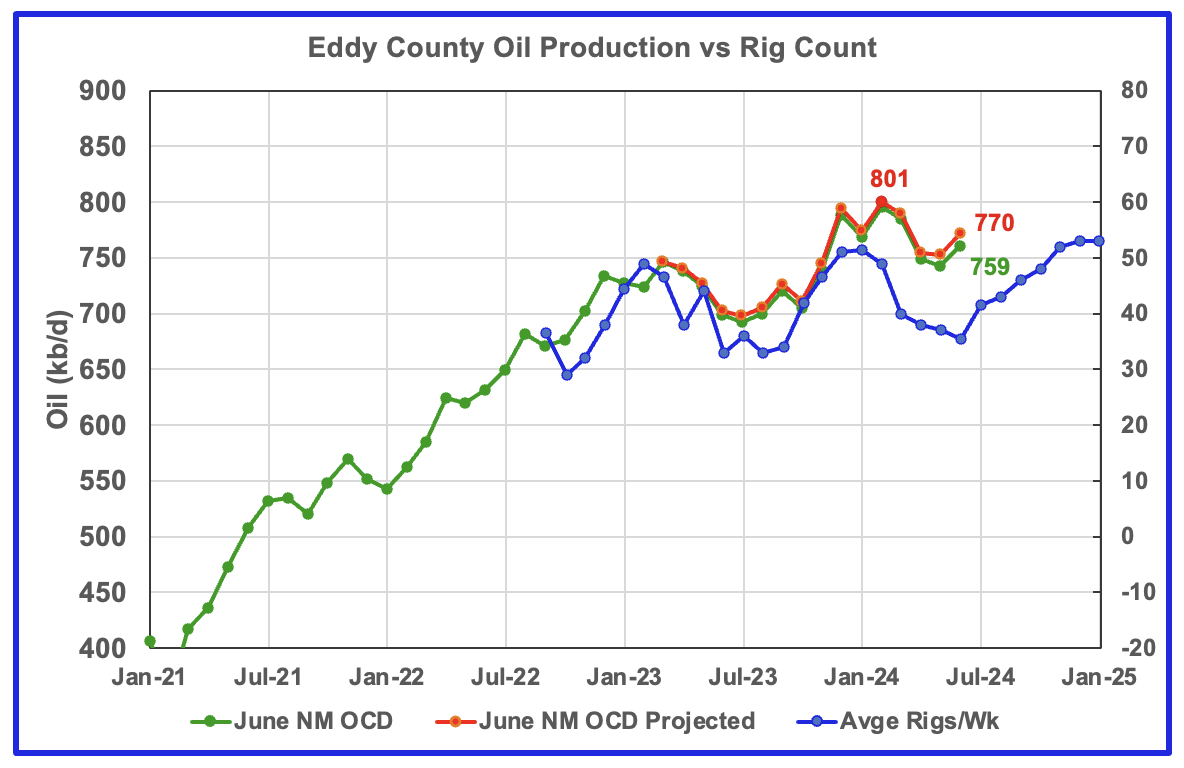

Eddy County oil production has peaked and appears to be tracking the rig graph.

Eddy county oil production hit a projected high of 801 kb/d in February 2024. The NM OCD projection estimates that the production forecast for June increased by 19 kb/d to 770 kb/d.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the above weekly drilling chart. The rig graph has been shifted forward by 8 months to roughly coincide with the increase in the production graph starting in October 2023.

If production were to follow the rig count trend going forward, Eddy production should continue to drop till June before rising again starting in July. However production began to rise in June. The beginning of a new rising trend does not mean that production will exceed the February peak of 807 kb/d. It is the increasing legacy decline that will limit how much production can increase from the May low.

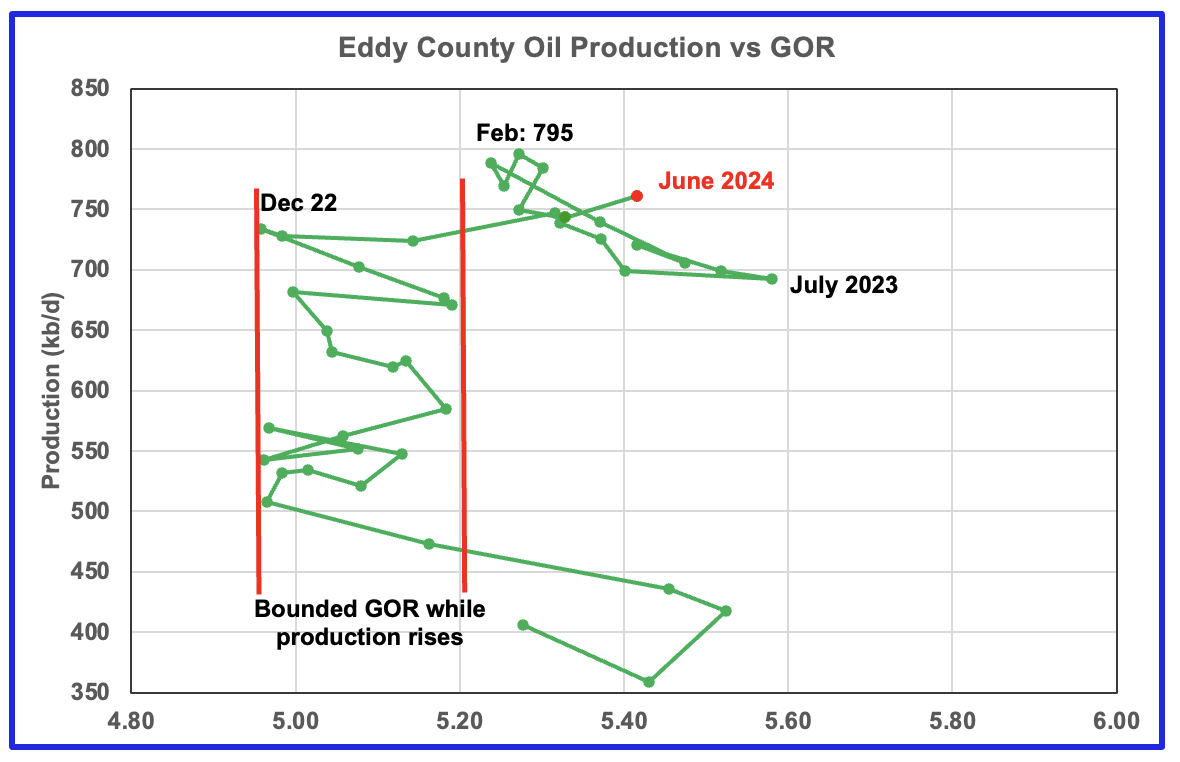

The Eddy county GOR pattern is similar to Lea county except that Eddy broke out from the semi bounded range earlier and for a longer time.

August 2023 saw a reversal in the increasing GOR trend which then was followed by the current oil production increase which reached a new high in February 2024 of 795 kb/d, an atypical pattern. This behaviour appears to be another bounded GOR phase while production rises.

Since February, production has fallen and the GOR has been essentially unchanged. For the last five months the GOR moved within a narrow range of 5.25 and 5.33. However June saw a jump in the GOR to 5.42 accompanied by a rise in production, red marker.

Texas Permian

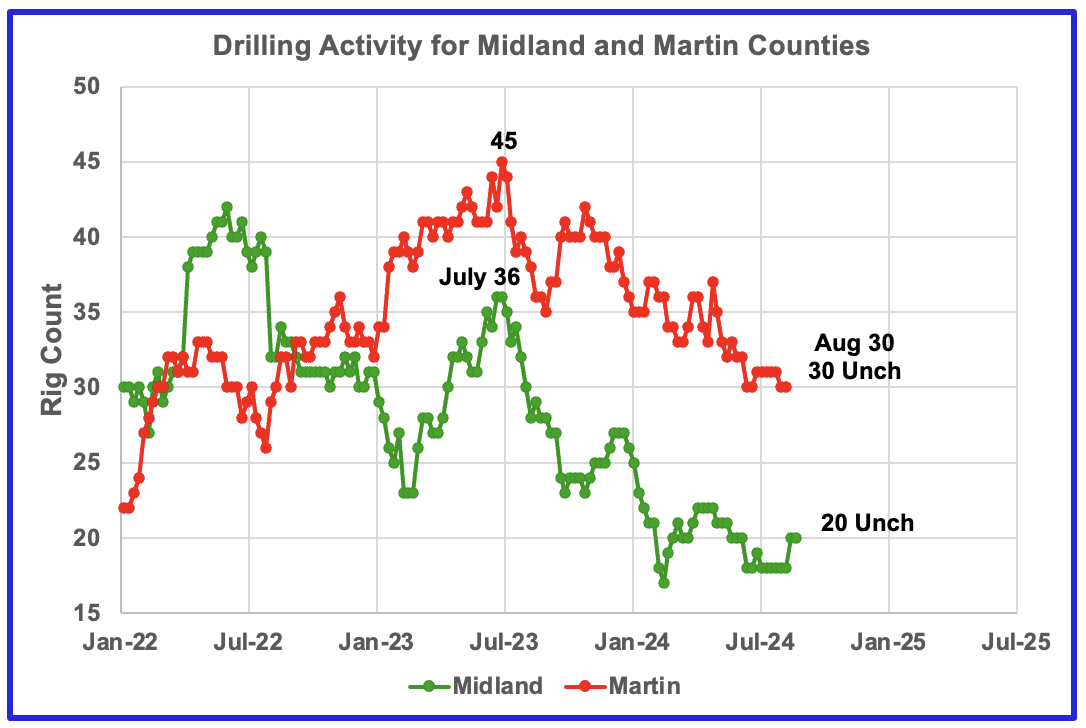

The rig count in Midland county has been dropping since July 2023. Midland county rigs have continued to drop and reached a low of 18 in July. They have rebounded to 20 at the end of August. Rigs are down close to 50% from where they were in July 2023.

Martin county rigs are also in a slow decline. At the end of August the rig count dropped another 2 to 30, down 33% from the high of 45 in July 2023.

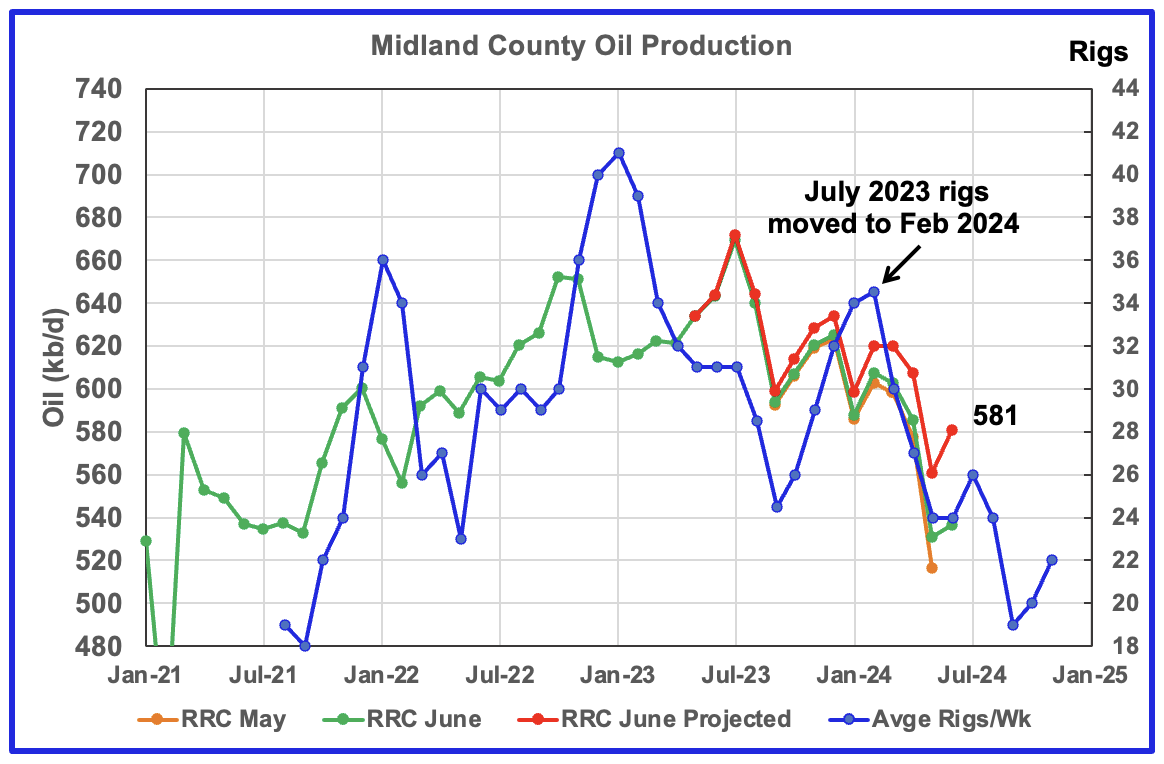

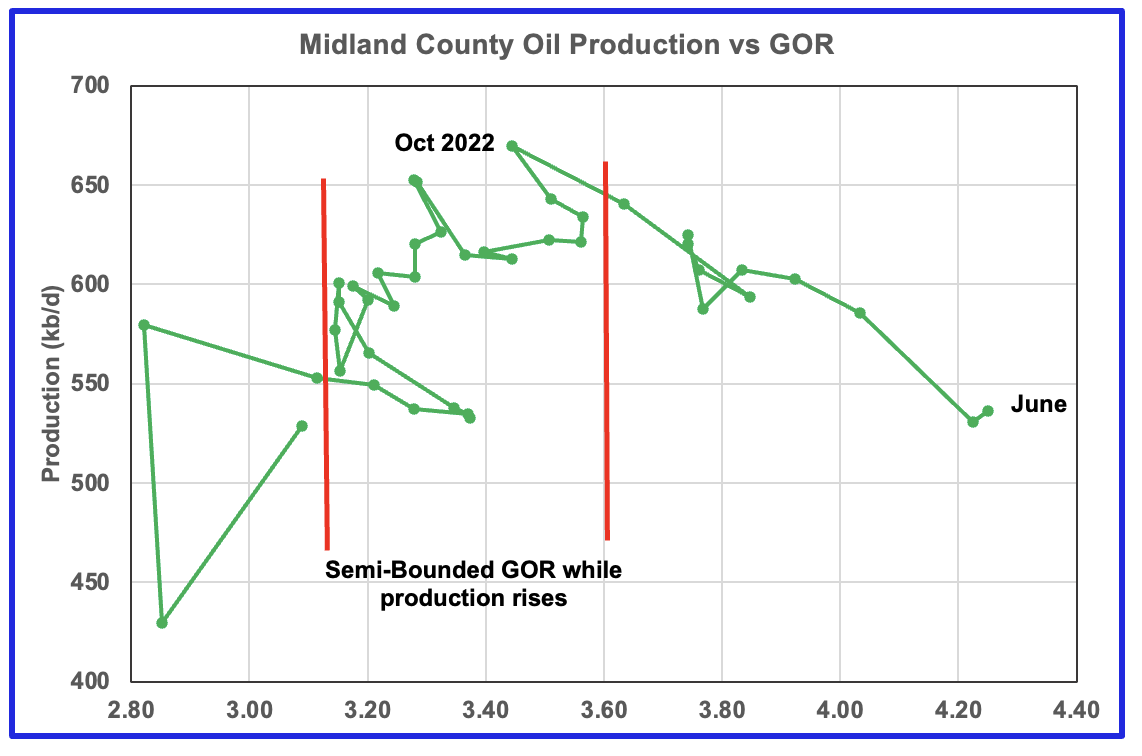

Midland County production has peaked.

Midland County’s slow and steady declining oil production phase started in August 2023. The green graph shows June’s preliminary production as reported by the Texas RRC. Midland county’s June preliminary production reversed the dropping trend and increased the projected production by 20 kb/d to 581 kb/d.

The orange and green graphs show the production reported by the Texas RRC for May and June. Note that the last month in the June production graph is higher than the last month in the May production graph. This is why the projection shows increased production for June.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the weekly drilling chart. The rig graph has been shifted forward by eight months. So the average 34.5 Rigs/wk operating in July 2023 have been moved forward to February 2024 to show the possible correlation and time delay between rig count and oil production. If the eight month shift in the rig count is approximately correct in that oil production can be tied to the rig count, oil production in Midland county should increase for a month or two before resuming its decline

With Midland county deep into the bubble point phase, oil production has dropped significantly from October 2022 and the GOR continues to increase. Note that oil production and GOR in this chart is based on the RRC’s preliminary May production report.

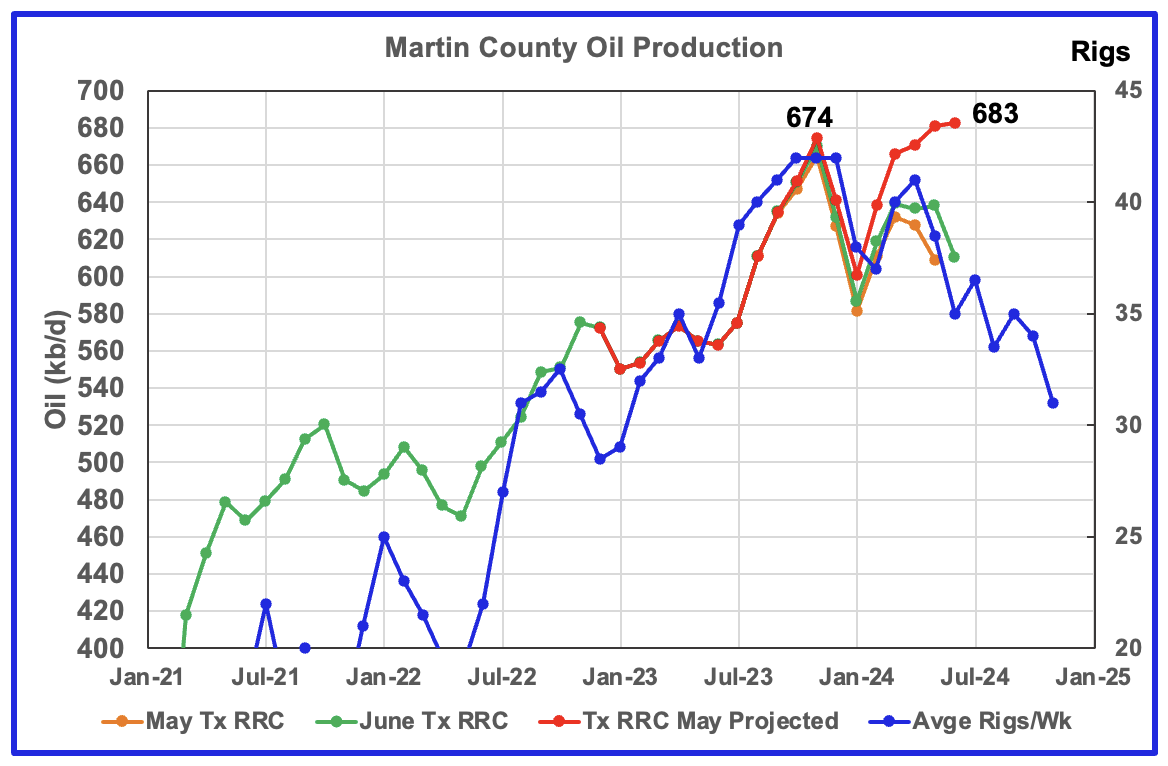

Martin County has peaked and is on a plateau and could be on the verge of entering its decline phase.

This chart shows Texas RRC oil production for Martin County. It was showing initial signs of peaking in November 2023 but was then followed by declining production to January 2024. Production has been tracking the increasing rig count according to the time shifted rig count and production began to increase in February. June production was essentially flat at 683 kb/d and is 9 kb/d higher than the November peak of 674 kb/d.

The red graph is a production forecast which the Texas RRC could be reporting for Martin county about one year from now as the Texas RRC reports additional updated production information. This projection is based on a methodology that used May and June production and will be re-estimated each month going forward. Production should fall in July if production follows the rig count.

The orange and green graphs show oil production reported by the Texas RRC for May and June.

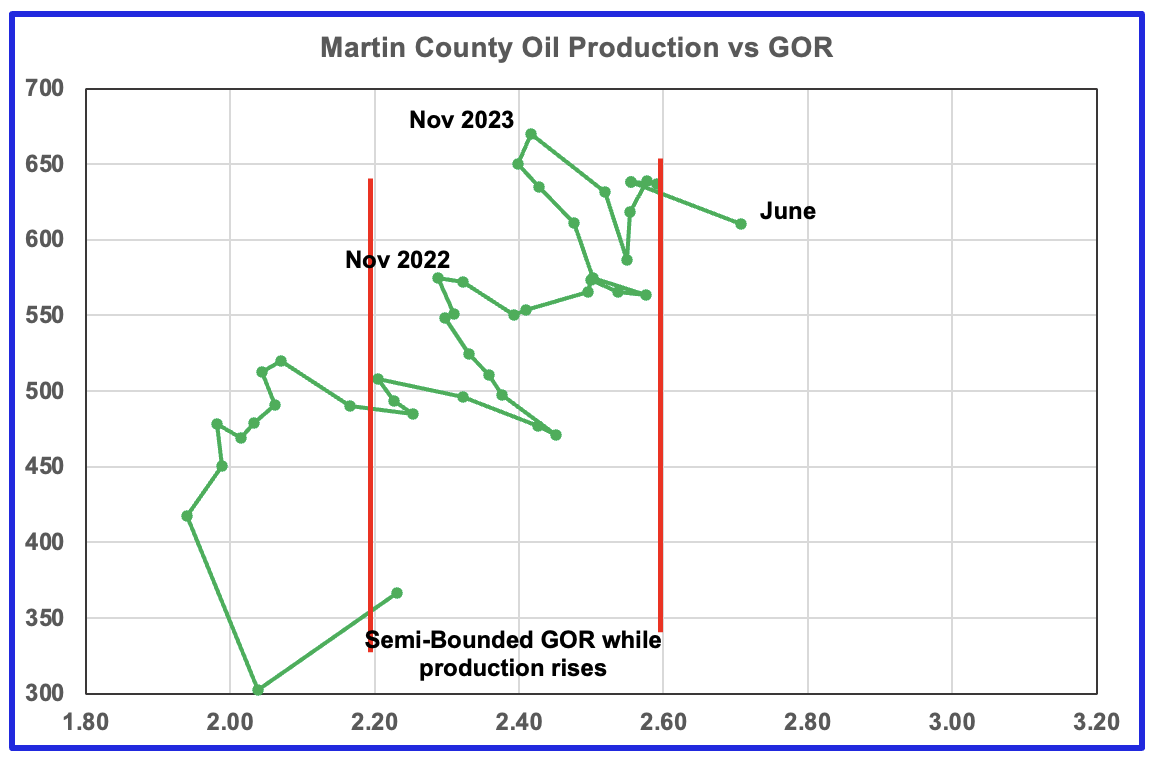

Martin county’s oil production after November 2022 increased and at the same time drifted to slightly higher GORs within the semi bounded range. However January, February and March 2024 saw production move higher while the GOR remained essentially unchanged at close to 2.56. June’s preliminary gas and oil production indicates that production was almost flat along with the GOR moving out of the semi-bounded area.

Martin county has the lowest GOR of the four counties at a GOR of close to 2.60 but for June jumped to 2.71, out of the semi-bounded region. Martin County may have entered the bubble point phase that should result in a dropping oil production trend.

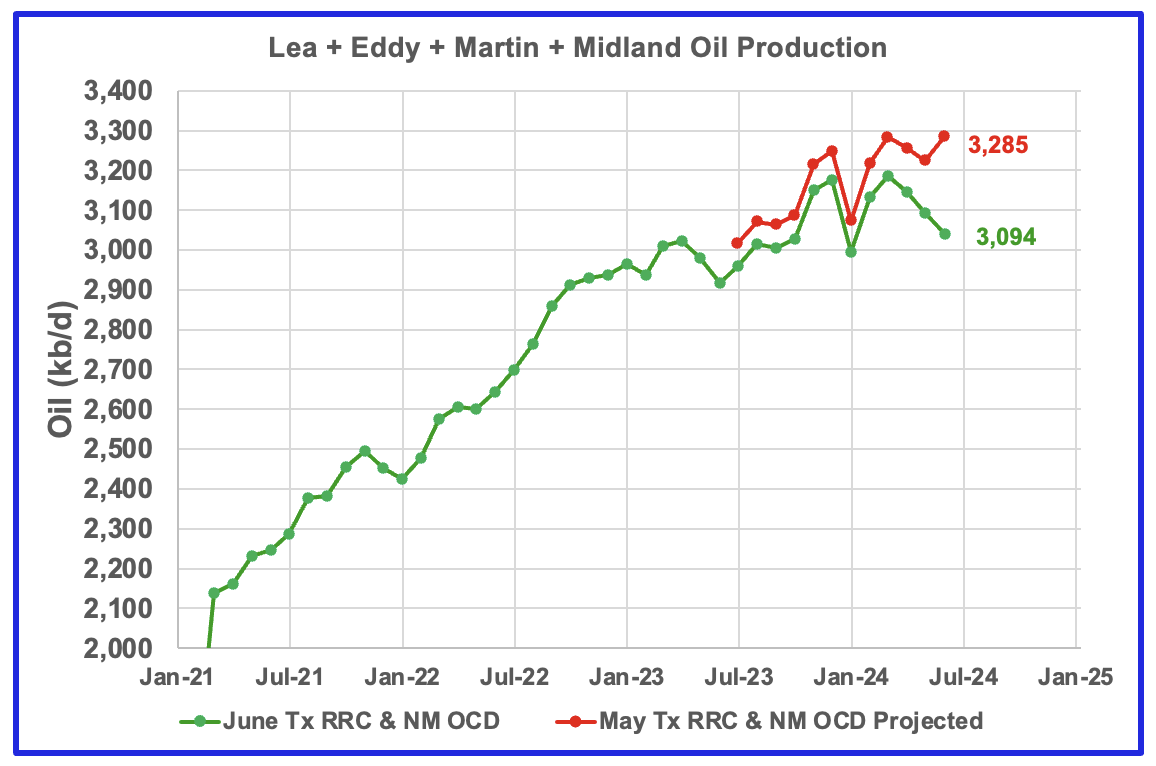

This chart shows the total oil production from the four largest Permian counties. Assuming that current June Permian production is close to 6,300 kb/d, these four counties account for 50% of the total. If their combined production has peaked, the Permian has peaked. A few more months of data is required to determine if the Permian has peaked.

June production rose by 60 kb/d to 3,285 kb/d. The May and June initial production data is shown in the orange and green graphs respectively. The red graph uses the May and June data to project an estimate for the final June production.

This chart is also affected by Lea update that made a total upward revision of 48 kb/d to production between March 2023 to June 2023. As such, we will have to wait for the July update to see whether the June increase in the projection is realistic.

Findings

– The Lea County oil production forecast was affected by revisions that will delay making a call on how close it is to peaking.

– Eddy County oil production peaked in February 2024 but has now started a new increasing phase as it follows the uptrend in the rig count.

– Midland county peaked in July 2023

– Martin County is on a plateau prior to heading into its decline phase.

A note on assumptions. In the above charts of production vs rig count, the rig count has been shifted forward by 7 to 8 months and the assumption is made that production follows rig count. The underlying assumption for doing that is that no more or very few DUCs are being used. Also implicit in making the above calls is that the drillers and frackers are using the latest technology, i.e. 3 mile laterals, max proppant and chemicals and some refracs. I have no basis for assuming this assumption is correct.

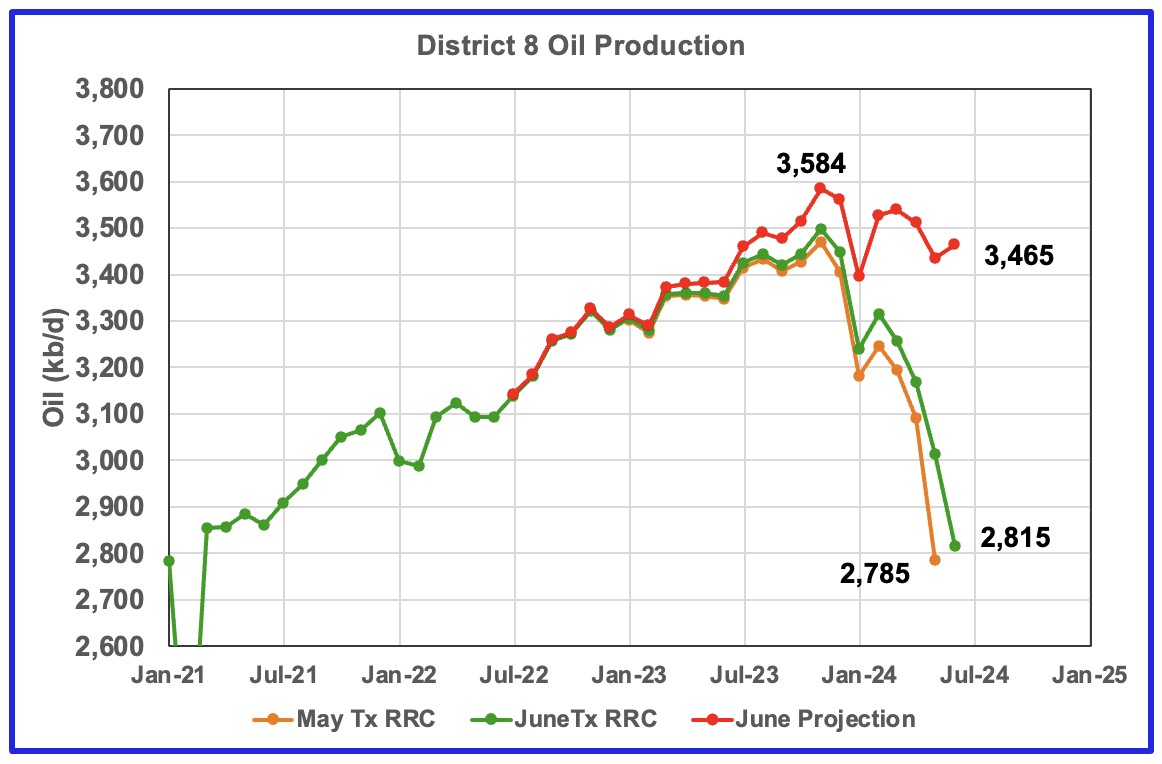

Texas District 8

Texas District 8 has peaked.

Texas District 8 contains both the Midland and Martin counties. Combined these two counties produce close to 1,300 kb/d of oil. While these two counties are the two largest oil producers, there are many other counties with smaller production, Reeves #3 and Loving #4, that resulted in total production of 3,584 kb/d in November 2023. Essentially the Midland and Martin counties produce close to 1/3 of the District 8 oil.

This chart shows a projection for District 8 oil production. The red graph, derived from the May and June production data indicates that oil production in District 8 has peaked. For June production rose by 30 kb/d to 3,465 kb/d and is down 119 kb/d from the peak in November 2023.

The orange and green graphs show the production reported by the Texas RRC for May and June. Note that the last month in the June production graph is higher than the last month in the May production graph. This is why the projection shows June’s production is higher than May’s.

District 8 accounts for more than half of Texas production. With June’s preliminary production being lower than November’s 3,584 kb/d, it is difficult to understand how the EIA’s Texas production has continued to increase since March.

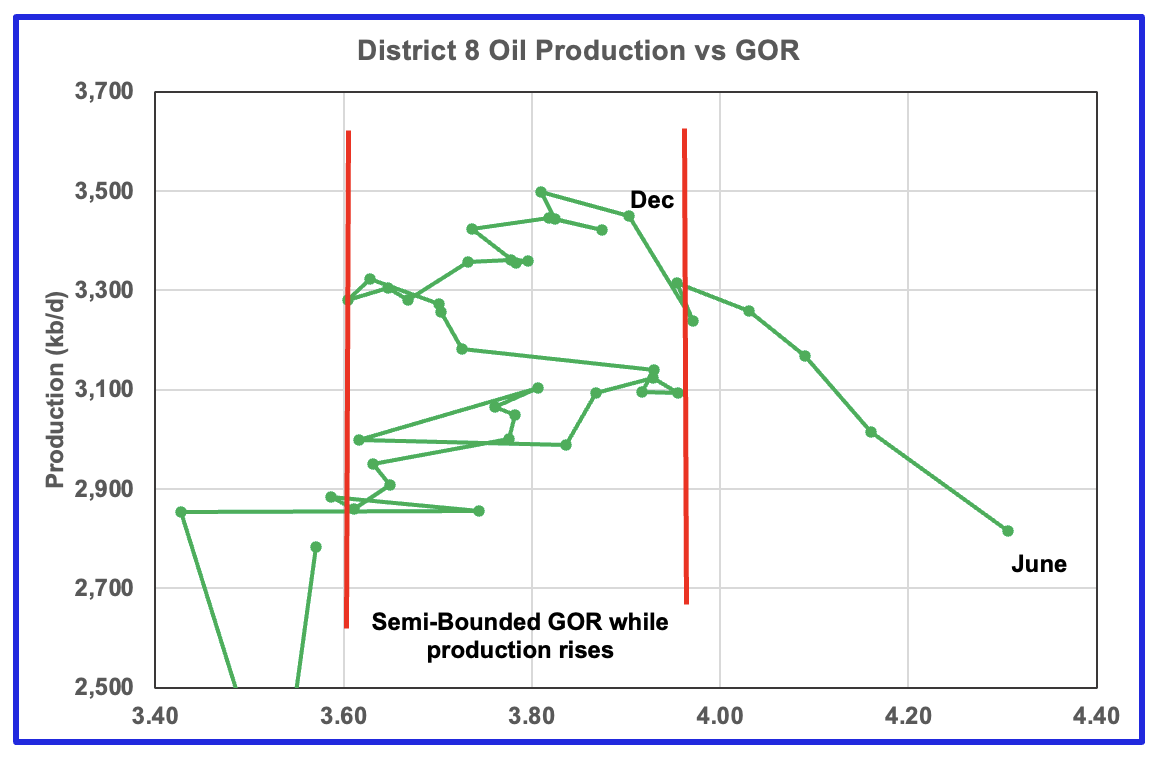

Plotting an oil production vs GOR graph for a district may be a bit of a stretch. Regardless here it is and it seems to indicate many District 8 counties may well be into the bubble point phase.

Drilling Productivity Report

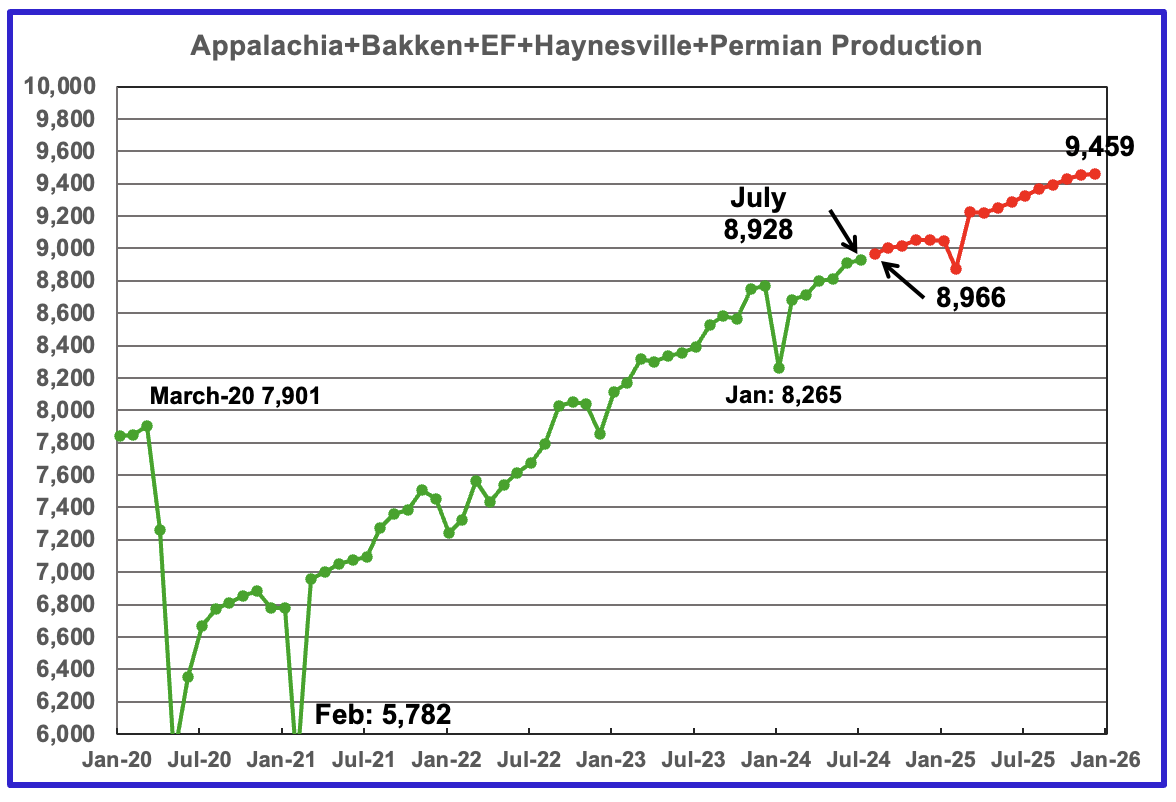

The Drilling Productivity Report (DPR) uses recent data on the total number of drilling rigs in operation along with estimates of drilling productivity and estimated changes in production from existing oil wells to provide estimated changes in oil production for the principal tight oil regions. The new DPR report in the STEO provides production up to July 2024 and is the first report to update the DPR production data since the format was changed. The report also projects output to December 2025. The DUC charts and Drilled Wells charts are also updated to July 2024.

The July 2024 oil production for the 5 DPR regions tracked by the EIA is shown above. Also a projection by the STEO to December 2025 has been added, red markers. Note DPR production includes both LTO oil and oil from conventional wells. Production for the Anadarko and Niobrara regions is no longer available.

The DPR is projecting oil output in July 2024 for these five regions will increase by 16 kb/d to 8,928 kb/d. Production is projected to grow almost linearly to 9,459 kb/d in December 2025. This is 180 kb/d lower than forecast in the July report.

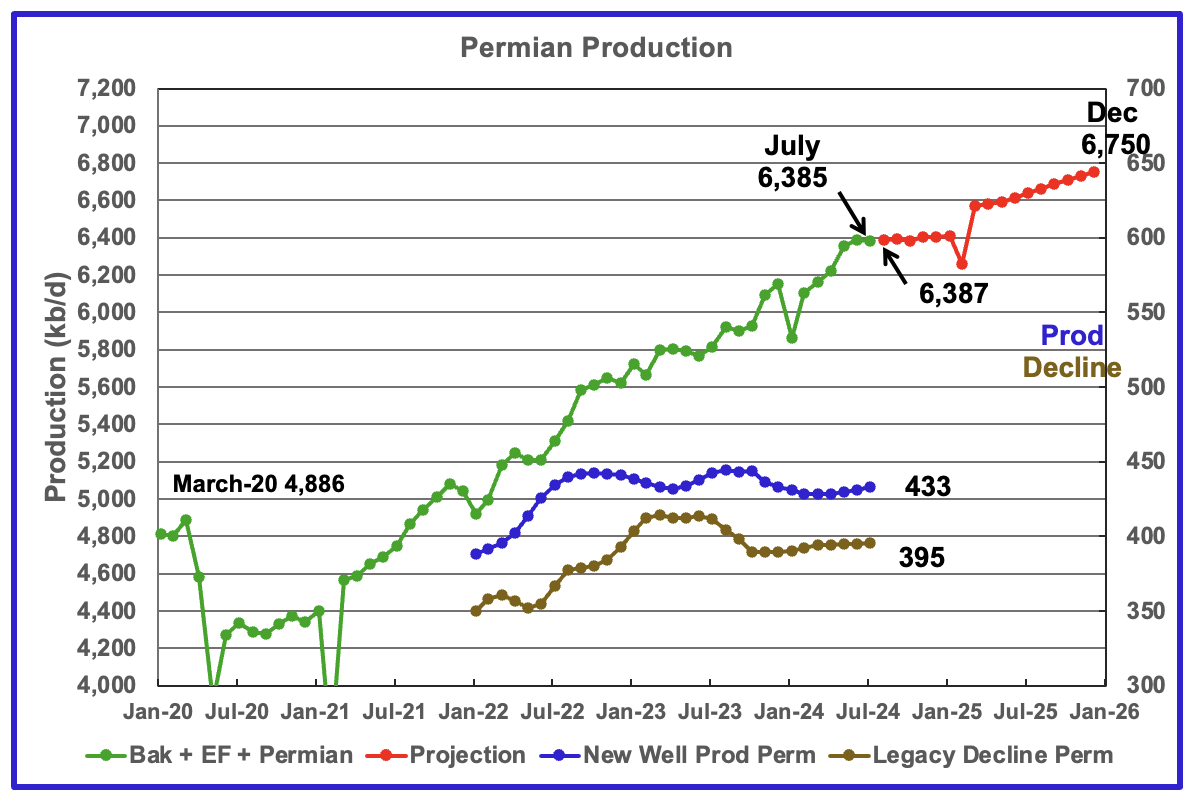

According to the EIA’s August DPR report, Permian output will be flat out to January 2025. It is expected to decrease by 5 kb/d to 6,385 kb/d in July. By December 2025 output is expected to be 6,750 kb/d, 144 kb/d lower than estimated in the previous report.

Production from new wells and legacy decline, right scale, have been added to this chart to show the difference between new production and legacy decline. For comparison, in the previous DPR report new well production was 443 kb/d, 10 kb/d higher than in the current report.

What is surprising is that production from new wells and legacy decline are different. They should be the same since production is flat? That has to make one question whether those numbers are correct?

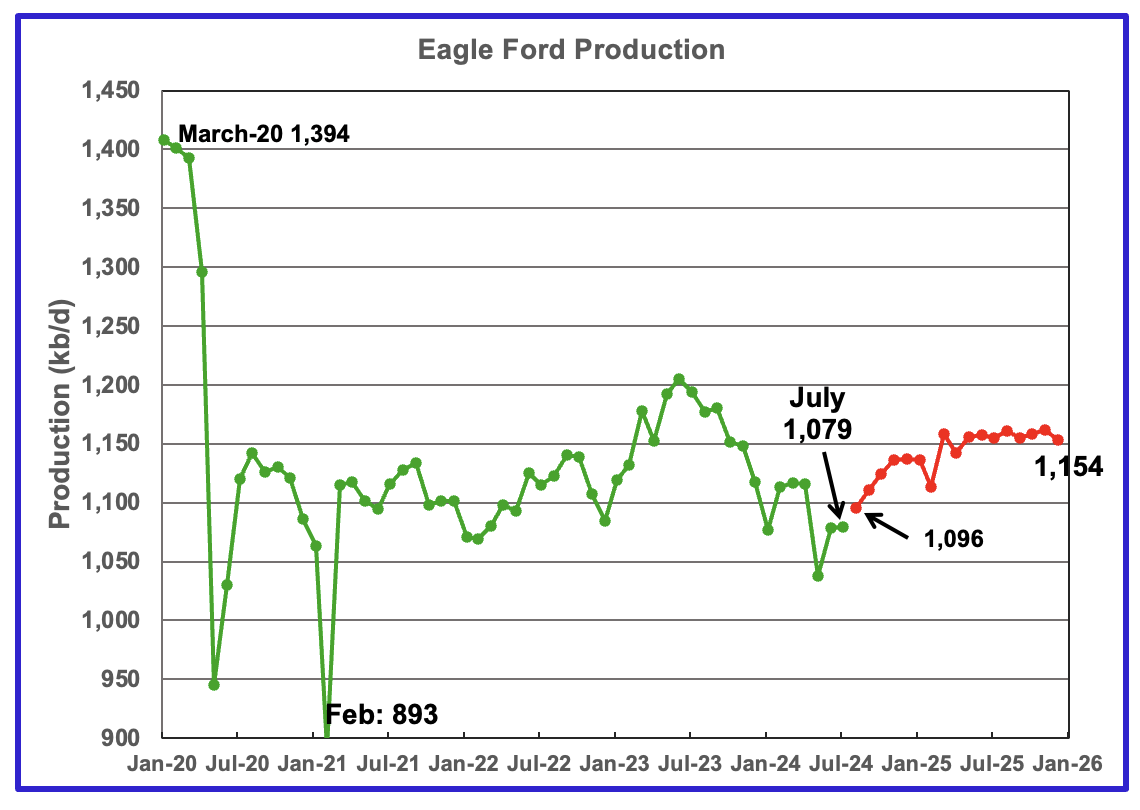

Output in the Eagle Ford basin has been declining since June 2023 but is expected to increase starting in August 2024. For July production is unchanged at 1,079 kb/d. However production is expected to reach close to 1,150 kb/d in March 2025 and remain there till December 2025. The red graph is a production projection by the STEO.

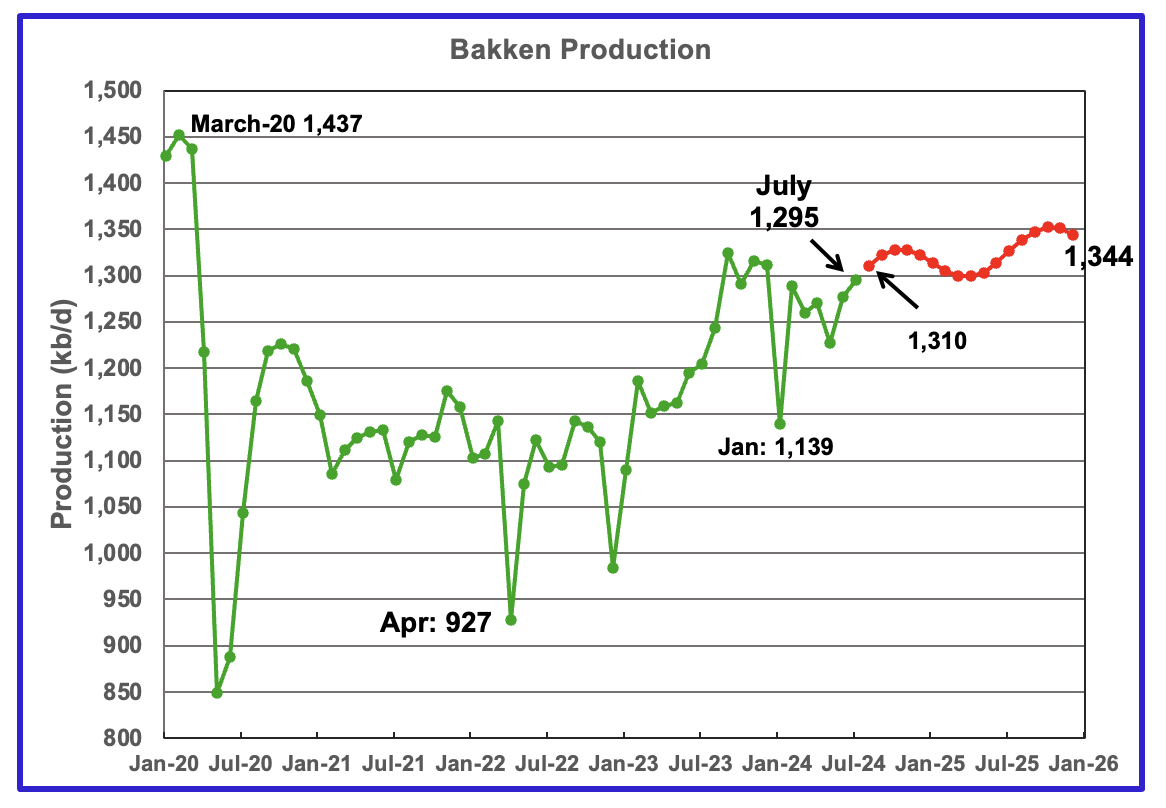

The DPR/STEO forecasts Bakken output in July will rise by 18 kb/d to 1,295 kb/d. The STEO projection out to December 2025 shows output varying between 1,300 kb/d and 1,350 kb/d over the next 18 months.

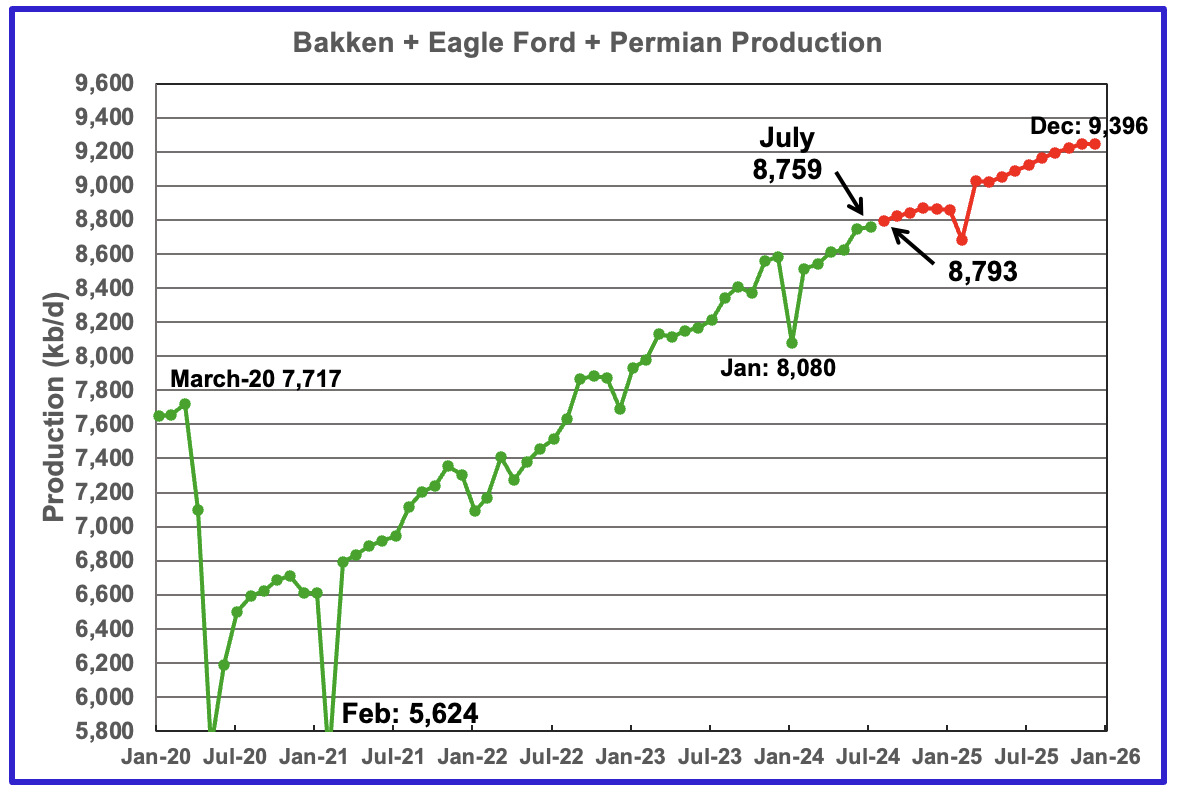

This chart plots the combined production from the three main LTO regions. For July output rose by 14 kb/d to 8,759 kb/d. Production in December 2025 is expected to reach 9,396 kb/d.

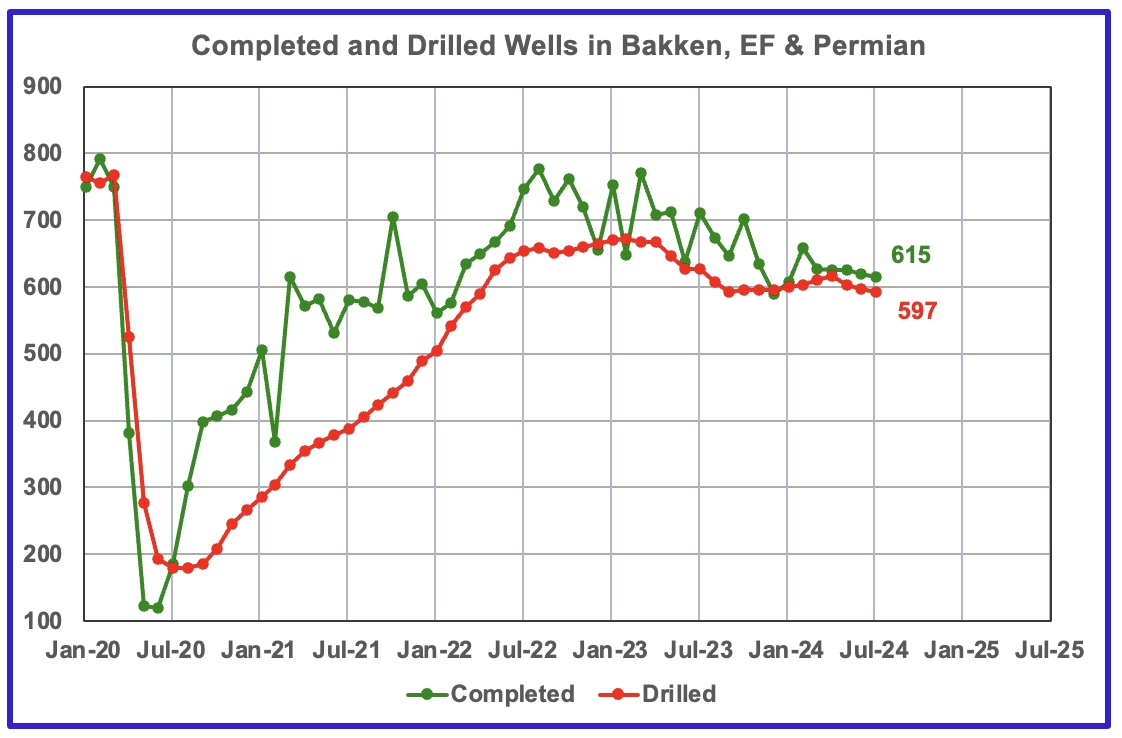

DUCs and Drilled Wells

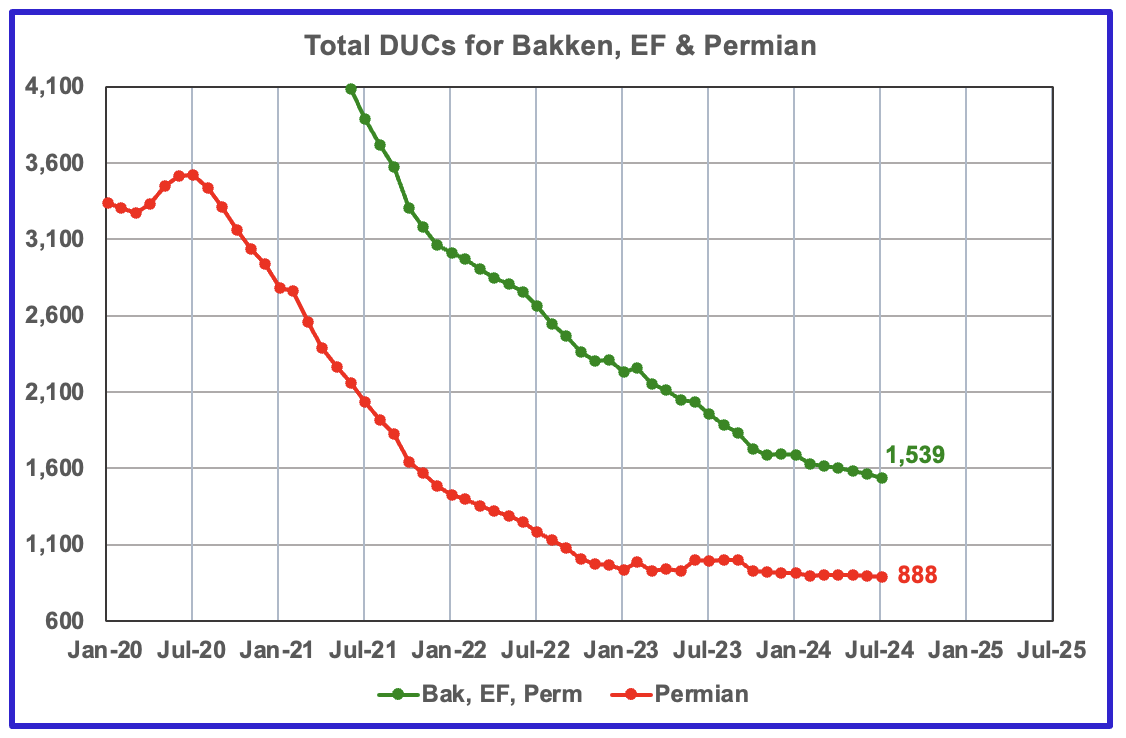

The number of DUCs available for completion in the Permian and the three major DPR regions has fallen every month since July 2020. July DUCs decreased by 22 to 1,539. In the Permian, the DUC count decreased by 7 to 888.

In the three primary LTO regions, 615 wells were completed and 597 were drilled. This indicates that there are still some profitable DUCs available.

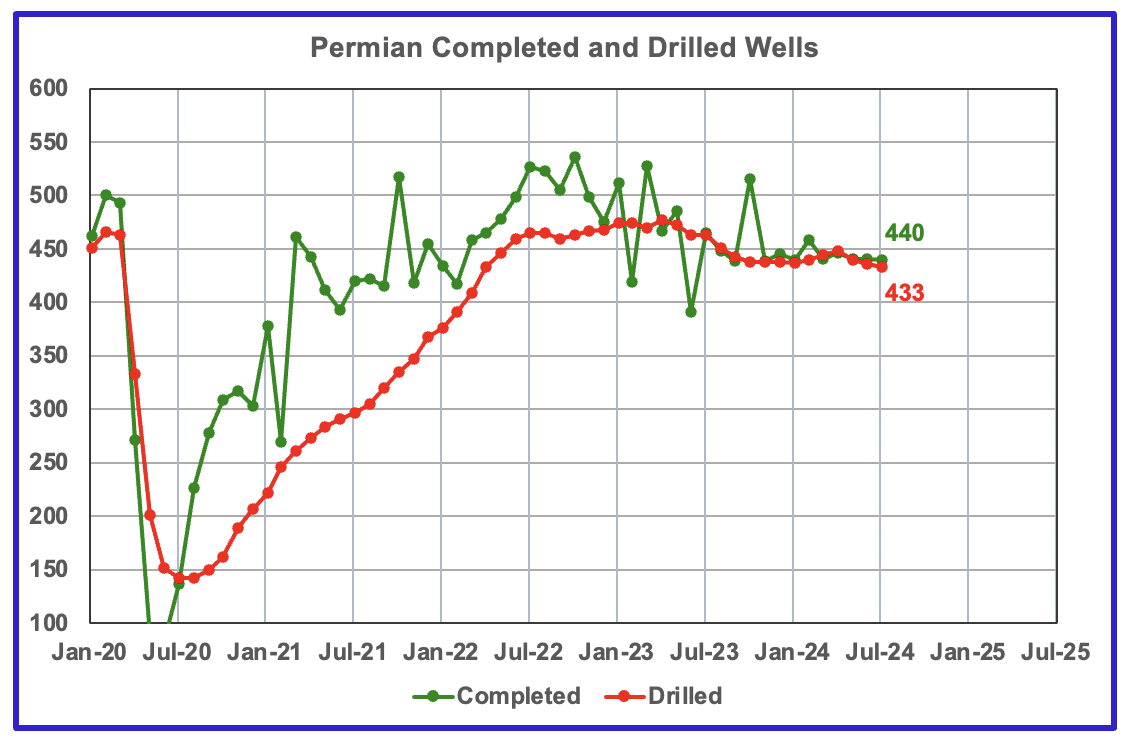

In the Permian, the monthly completion and drilling rates have been both stabilizing in the 430 to 450 range over the last eight months.

In July 2024, 440 wells were completed while 433 new wells were drilled. This is the third month in which the number of wells completed exceeded the drilled wells. Based on the DPR Permian chart above. it appears that these extra 7 completed wells are allowing production to stay on a plateau.